Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

During an earnings call in June 2025, KB Home’s McGibney—whose company prefers outright home price cuts over incentives when adjustments are needed—said that some buyers turning to competitors are effectively overpaying for new builds to obtain mortgage rate buydowns. If those buyers need to sell in the near term, he warned, they could find themselves underwater and unable to recoup the artificially high base prices.

“I believe that there are [builder] customers that are overpaying for the home to effectively get an incentive… They may potentially be upside down when they try to sell that home,” McGibney said back in June.

In January 2026, ResiClub interviewed KB Home CEO Jeffrey Mezger and COO Rob McGibney—beginning March 1, 2026, McGibney will assume the CEO role. During that conversation, ResiClub asked KB Home about that upside-down comment.

Mezger and McGibney reaffirmed their stance, saying they’ll continue to lean into “transparent” pricing over incentives.

“We believe in price transparency,” Mezger tells ResiClub. “Our biggest competitor is resale—and [resale] sellers don’t offer incentive packages.”

In the view of KB Home executives, leaning too hard into incentive-driven strategies—when affordability adjustments or net effective price cuts are needed to meet the market—can translate into inflated base prices, larger loan balances, and greater near-term resale risk if a buyer needs to move sooner than expected.“Our buyers tell us they like the clarity,” McGibney tells ResiClub. “They [our buyers] know exactly what they’re paying for… I think [transparent pricing] really lowers that risk of [the buyer] overpaying for a home and potentially being upside down.”

Not long after mortgage rates spiked in 2022 and the pandemic housing boom fizzled out, many large homebuilders began offering sizable mortgage rate buydowns. Some have gone as far as shelling out $40,000, $50,000, or even $60,000 toward “forward commitments” that can get a borrower’s mortgage rate below 4.99%—or even 3.99%. Through an economic lens, the homebuyer is still ultimately paying for those buydowns if the headline price isn’t coming down.

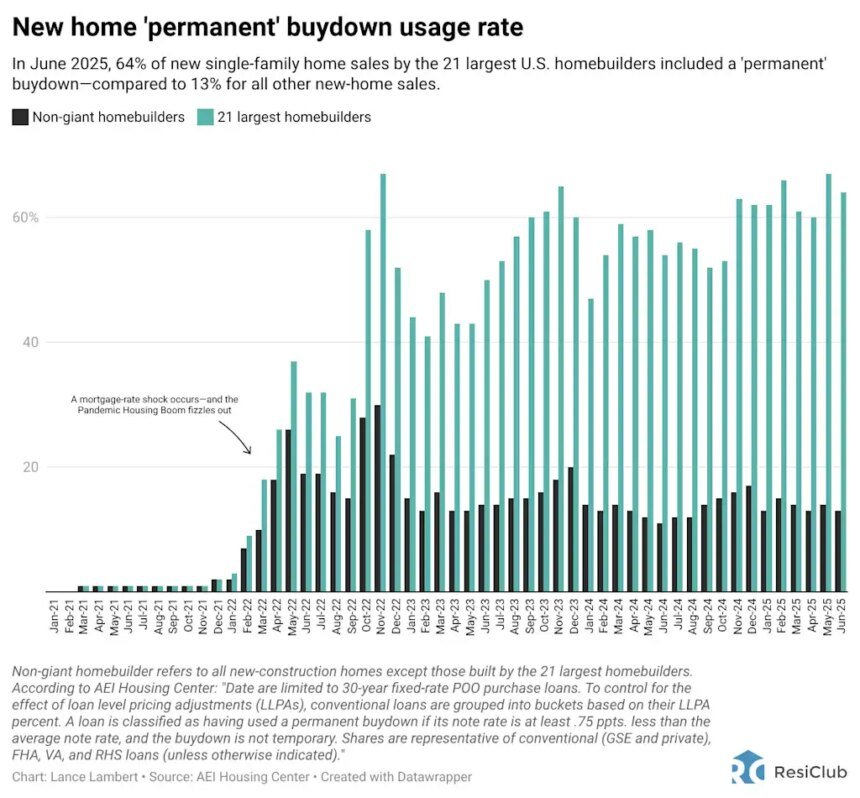

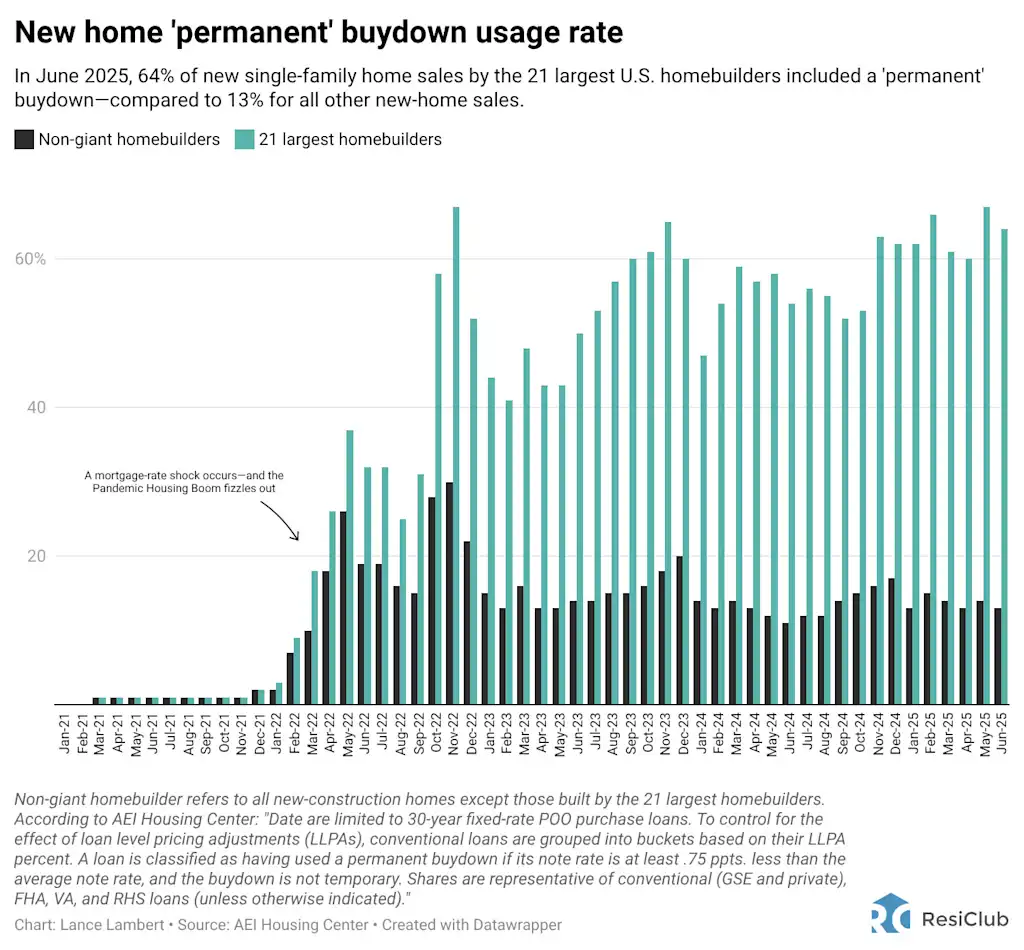

According to AEI Housing Center, 64% of new single-family home sales in June 2025 by the 21 largest U.S. homebuilders included a “permanent” buydown—compared with 13% for all other new-home sales. Many large homebuilders do this because arbitrage in the bond market allows them to achieve a marginally larger reduction in a buyer’s monthly payment for each dollar spent on mortgage rate buydowns than for each dollar spent on outright price cuts.

Here’s what Edward Pinto, senior fellow and co-director of the AEI Housing Center, wrote in a report published in November 2025:

“Why don’t [more] builders just cut prices instead? The main reason is that permanent buydowns are far more cost-effective… lowering the rate [via forward commitments for buydowns] by 100 bps costs the builder roughly 3.2% of the sale price. To achieve the same monthly payment through a direct price cut, the builder would need to cut the price by 10%. Furthermore, once a builder cuts the price on one home, buyers would expect similar discounts for the entire subdivision. But there is another factor at work. Permanent buydowns funded through bulk forward commitments are excluded from the seller concession limits, which cap how much a seller can contribute toward the borrower’s closing costs. For Fannie Mae and Freddie Mac seller concessions are generally limited to 3-6% and for FHA the limit is generally 6%. Over 40% of sales by large builders have a combination of seller concessions plus permanent buydown cost in excess of 6%.”