Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

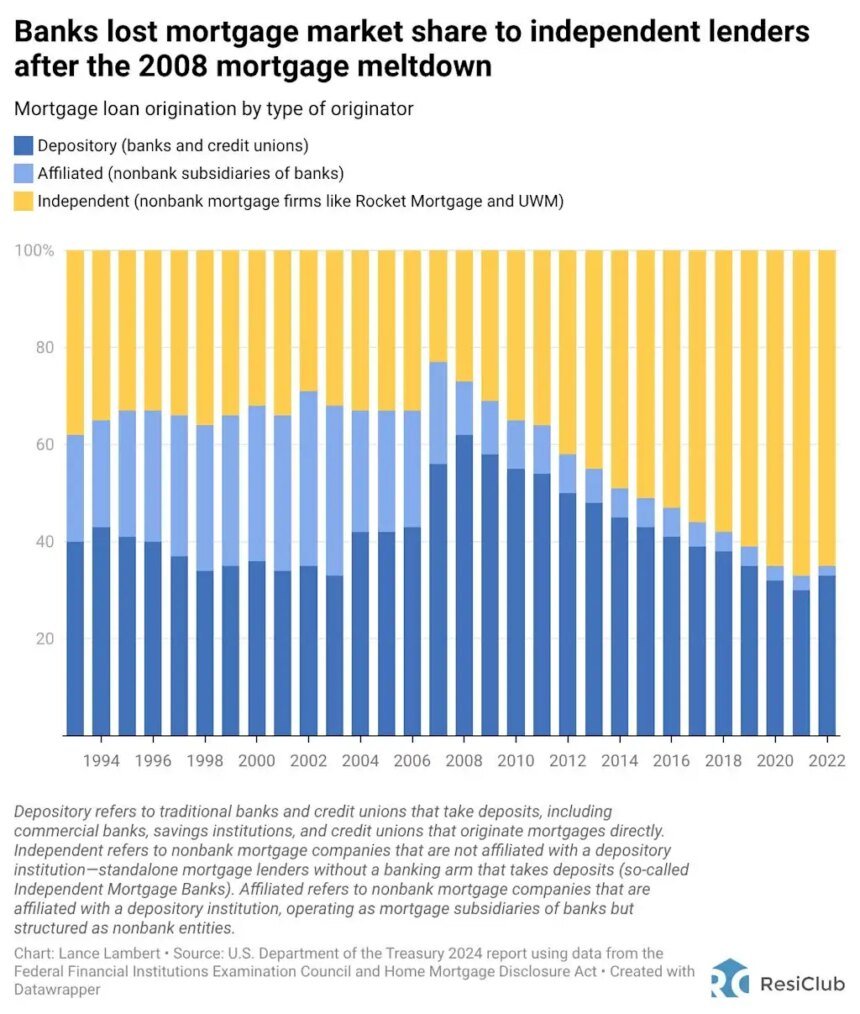

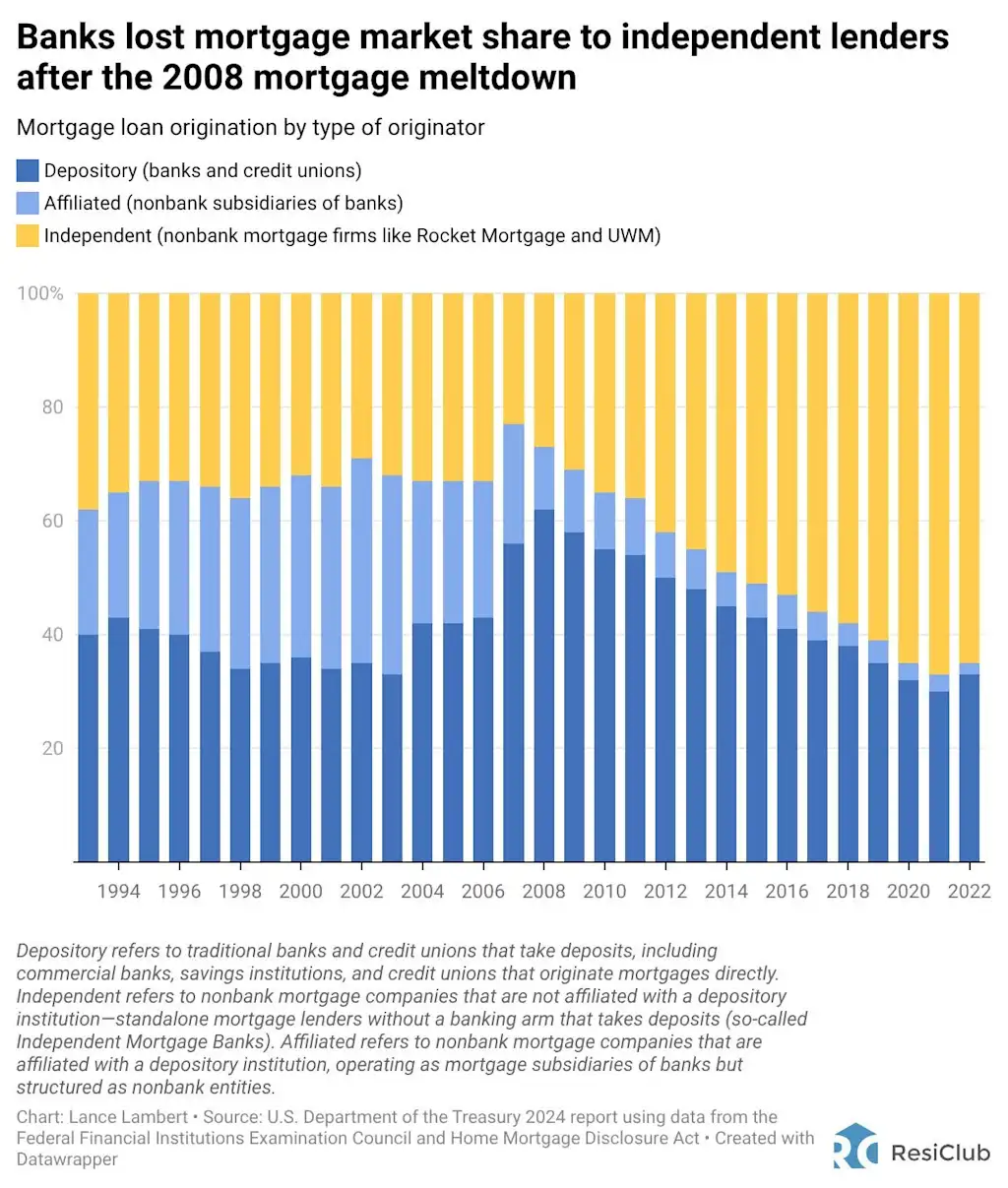

Since the 2008 housing bust and subsequent Great Financial Crisis (GFC), mortgage lending has steadily shifted away from big banks. In the years that followed—amid tighter regulations, higher capital requirements, and elevated litigation risk—many large banks, including Bank of America, JPMorgan Chase, and Wells Fargo, reduced their mortgage footprint. In that void, nonbank lenders, also known as independent mortgage banks (IMBs), such as Rocket Mortgage, United Wholesale Mortgage (UWM), and loanDepot, gained market share.

Now, a top Federal Reserve official is openly questioning whether policy and regulation went too far—and is signaling that a policy shift may be coming.

In a February 16 speech at the American Bankers Association’s Community Bankers Conference, Federal Reserve Vice Chair for Supervision Michelle Bowman pointed to what she described as a “significant migration” of mortgage origination and servicing out of the banking sector over the past 15 years.

According to Bowman:

- In 2008, banks originated around 60% of mortgages and held the servicing rights on about 95% of mortgage balances

- In 2023, banks originated around 35% of mortgages and held the servicing rights on about 45% of mortgage balances

That’s pretty in line with the data ResiClub pulled from the U.S. Department of the Treasury:

During her speech, Bowman suggested that post-2013 capital rules—particularly the treatment of Mortgage Servicing Rights (MSRs)* under Basel standards**—may have contributed to the mortgage retreat by banks. MSRs, which represent the expected value of servicing income when loans are sold into securitizations, were assigned higher risk weights and subject to deduction thresholds after the crisis. While regulators tightened those rules over concerns about valuation volatility and model risk, the capital treatment also made servicing and, by extension, mortgage origination less economically attractive for banks.

The result, Bowman implied, is a mortgage market increasingly concentrated in nonbank firms that lack deposit funding and operate under different supervisory and resolution frameworks. During the COVID-19 lockdowns, Bowman said, borrowers with bank servicers were more likely to receive forbearance than those serviced by nonbanks—highlighting structural differences that can matter during stress periods, she says.

Bowman previewed potential changes now under consideration, including removing the deduction requirement for MSRs and making mortgage capital rules more sensitive to loan-to-value ratios rather than applying a uniform risk weight. Such changes would not unwind post-crisis reforms but could modestly improve the economics of bank mortgage activity, Bowman says.

Here’s what Bowman said in her February 16 speech:

“Two regulatory proposals will soon be introduced that, among other broader changes to the regulatory capital framework, would increase bank incentives to engage in mortgage origination and servicing. First, the proposals would remove the requirement to deduct mortgage servicing assets from regulatory capital while maintaining the 250 percent risk weight assigned to these assets. We will seek comment on the appropriate risk weight for these assets. This change in the treatment of mortgage servicing assets would encourage bank participation in the mortgage servicing business while recognizing uncertainty regarding the value of these assets over the economic cycle. Second, the proposals would also consider increasing the risk sensitivity of capital requirements for mortgage loans on bank books. One approach would be to use loan-to-value ratios to determine the applicable risk weight for residential real estate exposures, rather than applying a uniform risk weight regardless of LTV. This change could better align capital requirements with actual risk, support on-balance-sheet lending by banks, and potentially reverse the trend of migration of mortgage activity to nonbanks over the past 15 years.”

James Kleimann, founder of Mortgage Scoop, writes the following:

“This stuff is quite complicated, but basically the Fed is weighing a plan to remove the rule that banks must deduct MSR assets from regulatory capital while maintaining a 250% risk weight for those assets. In plain English, that means regulators treat $1 of MSRs like $2.50 of risky assets. What the appropriate risk weight level should be remains the central question, but this potential change is something the MBA [Mortgage Bankers Association] has been arguing in favor of for years.”

Big picture: If adopted, the proposals could mark the beginning of a gradual rebalancing in housing finance—one that brings more mortgage origination and servicing back inside the traditional banking system after more than a decade of migration outward.