Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

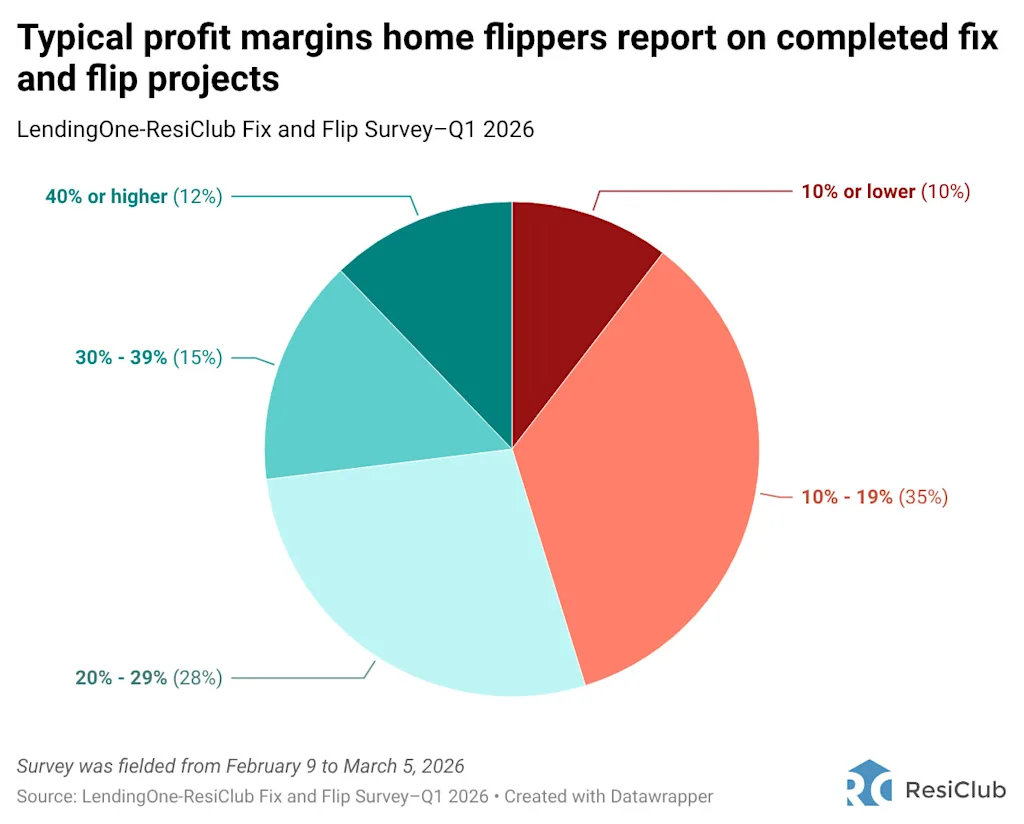

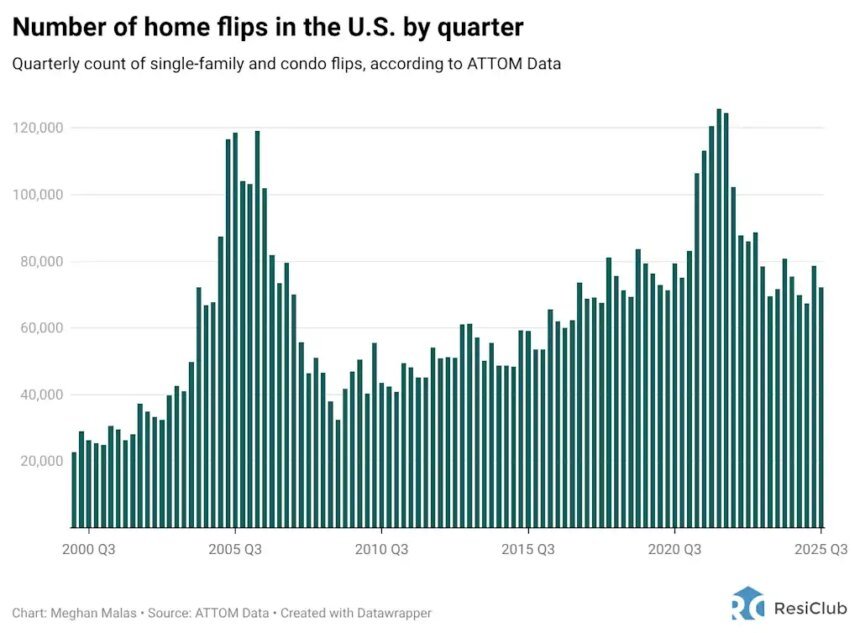

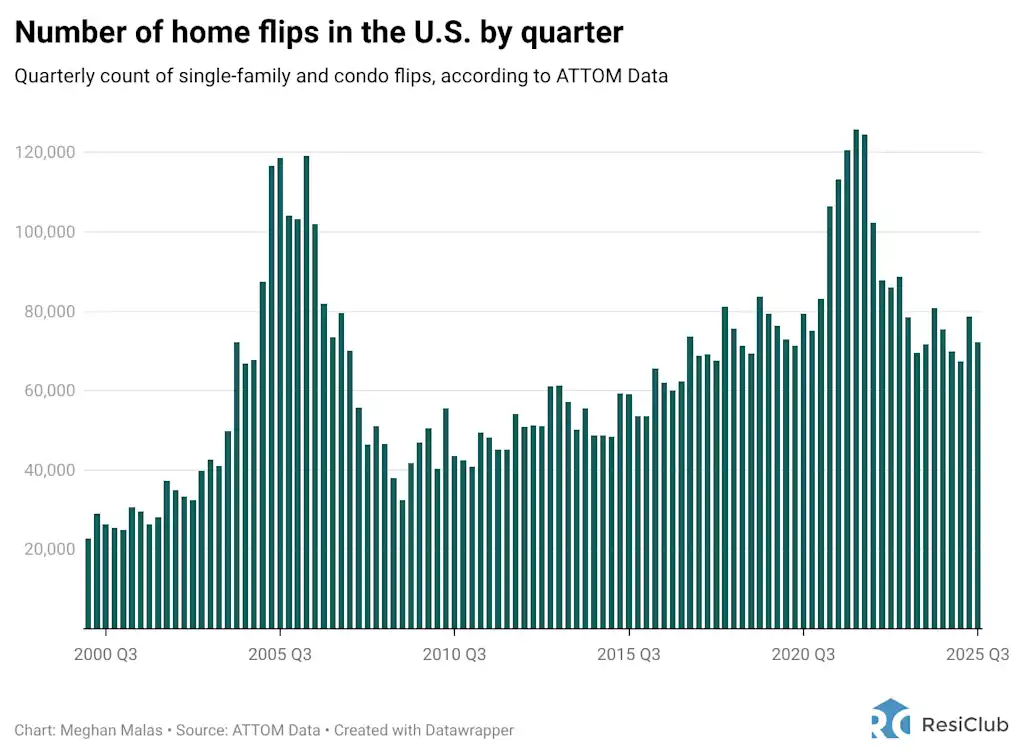

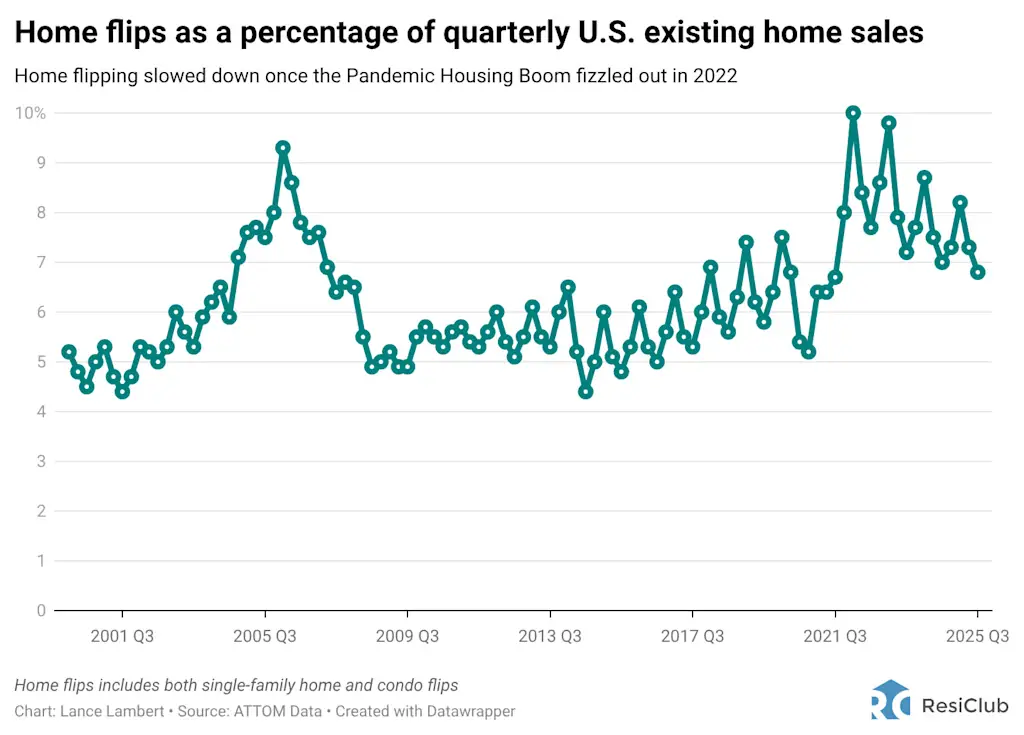

During the Pandemic Housing Boom, rapid home price appreciation supercharged fix-and-flip activity. The 2022 mortgage rate shock ended that run and caused the biggest pullback in home flipping activity since 2007. Profit margins compressed, days on market increased, and many newer investors exited the space.

However, over the past couple of years, home flipping activity has stabilized around 2019 levels.

The first LendingOne–ResiClub Fix-and-Flip Survey in Q1 2025 showed a market recalibrating to that new reality. The latest results tell a similar story: Flipping activity has stabilized, and seasoned flippers are still planning to execute deals in 2026—even in a slower national appreciation environment.

Today, we’re breaking down the full results from the LendingOne–ResiClub Fix and Flip Survey for Q1 2026, fielded between February 9 and March 5, 2026. In total, 201 home flippers took the survey. The data suggest the market remains steady: demand expectations are holding up across many regions, and margins—while no longer pandemic-level—remain workable for disciplined flippers.

1. Home flipper sentiment and intent

Shifts over the past year:

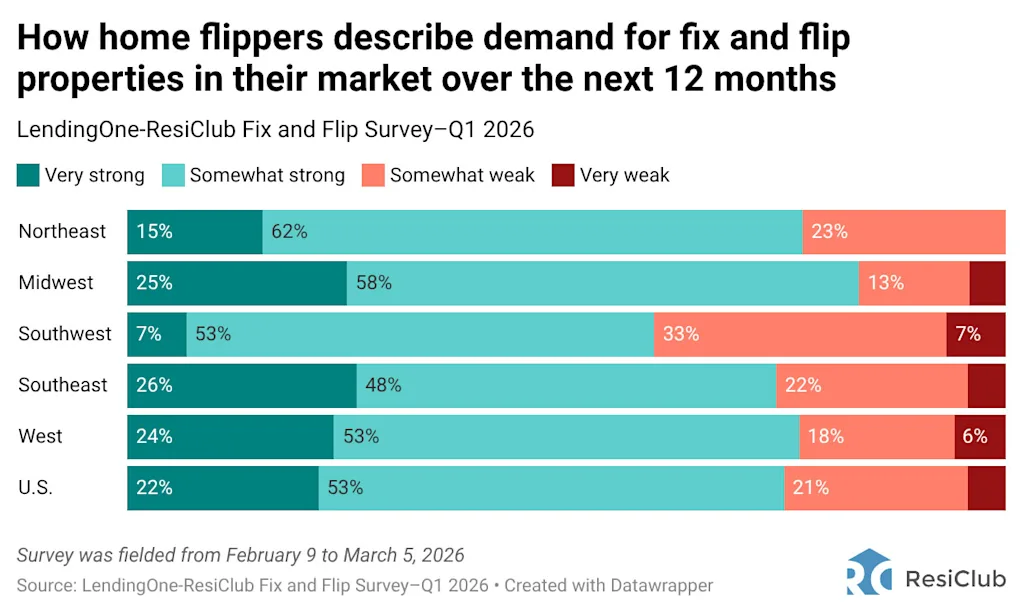

- Market sentiment has remained steady over the last year: 53% of U.S. home flippers describe their primary market as somewhat strong (44%) or very strong (9%), compared to 56% in Q3 2025 and 54% in Q1 2025.

- Expectations for demand remain resilient: 75% of flippers expect somewhat strong (53%) or very strong (22%) demand over the next 12 months, compared to 72% in Q3 2025.

Fix and flip activity:

- A strong majority of flippers (90%) say they are somewhat or very likely to conduct a fix and flip in the next 12 months, including 75% who say they are “very likely.”

- Just over half (52%) plan to convert 1 to 5 projects into rentals using the fix-to-rent method, while 38% do not plan to convert any projects.

- Home flippers in the Midwest are the most confident in buyer demand, with 83% describing conditions as either somewhat strong or very strong—the highest share of any region.

Market outlook:

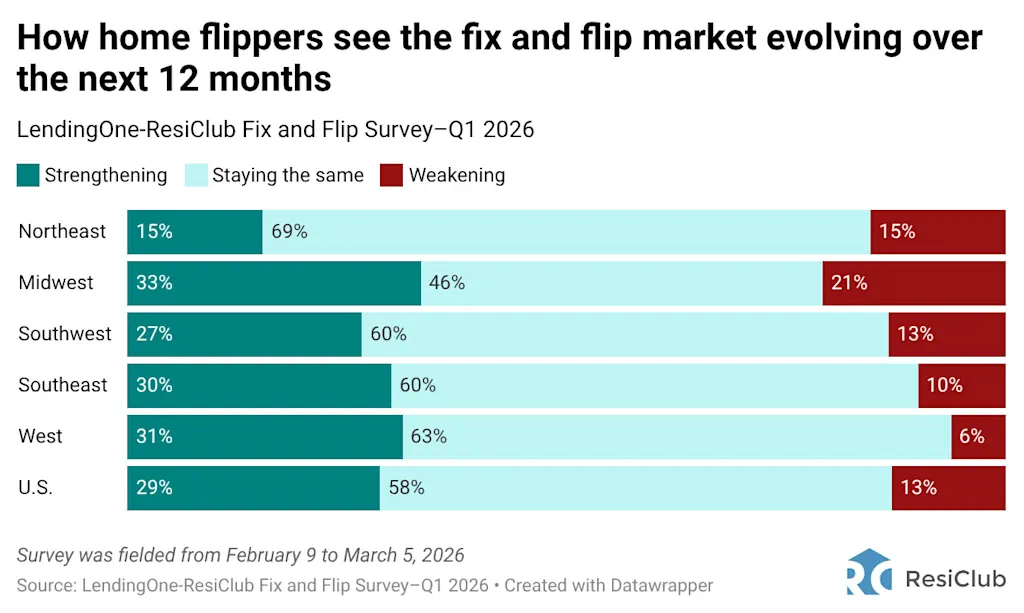

- 58% of survey participants expect the fix and flip market to stay the same over the next 12 months, compared to 42% in Q3 2025.

- 29% expect the market to strengthen, compared to 31% in Q3 2025.

- 13% expect the market to weaken, down from 22% in Q3 2025.

- Optimism runs highest in the Midwest (33% expect strengthening) and West (31%), while the Northeast shows the highest weakening share (15%).

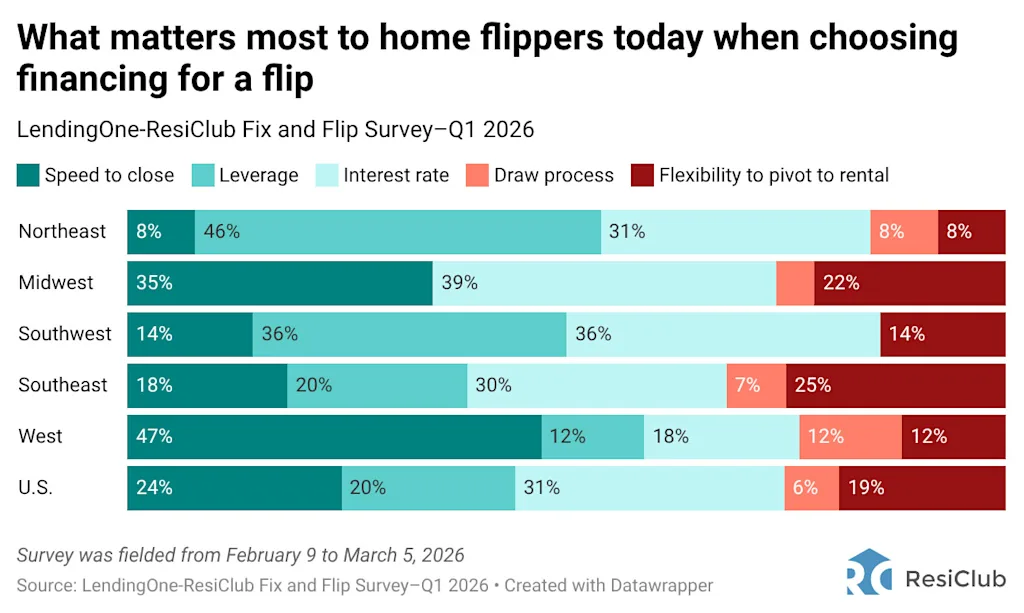

2. Financial considerations

Leverage:

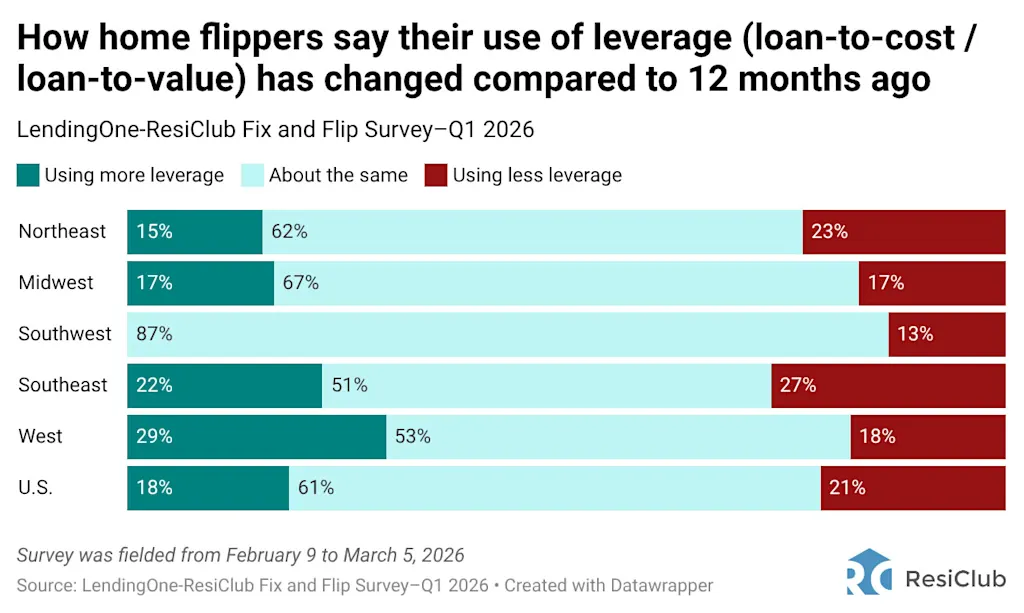

- 61% of U.S. home flippers say their use of leverage is about the same compared to 12 months ago, meanwhile, 21% say they are using less leverage, and 18% say they are using more.

Financing priorities:

- Interest rate (31%) and speed to close (24%) are the top considerations when choosing financing.

- Speed to close (47%) is overwhelmingly the top consideration reported by home flippers in the West.

3. The biggest concerns across U.S. markets

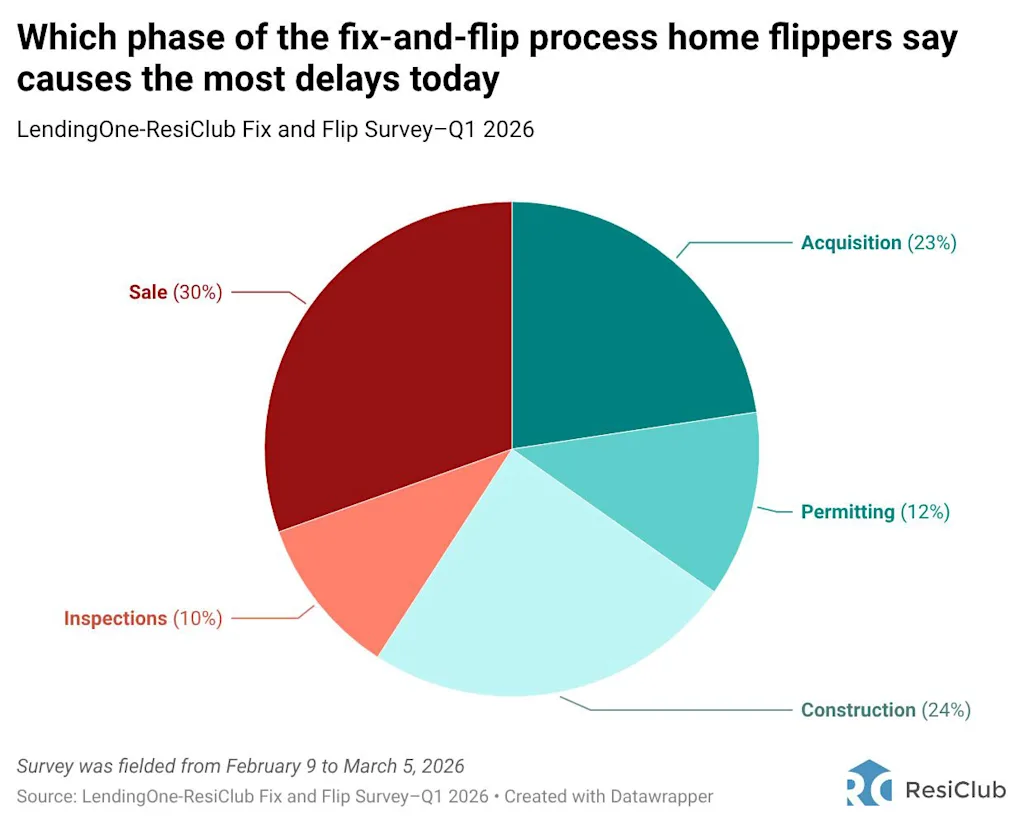

Organization and timeline stress:

- The sale phase causes the most delays (30%) for U.S. home flippers, followed by rehabbing/construction (24%) and acquisition (23%).

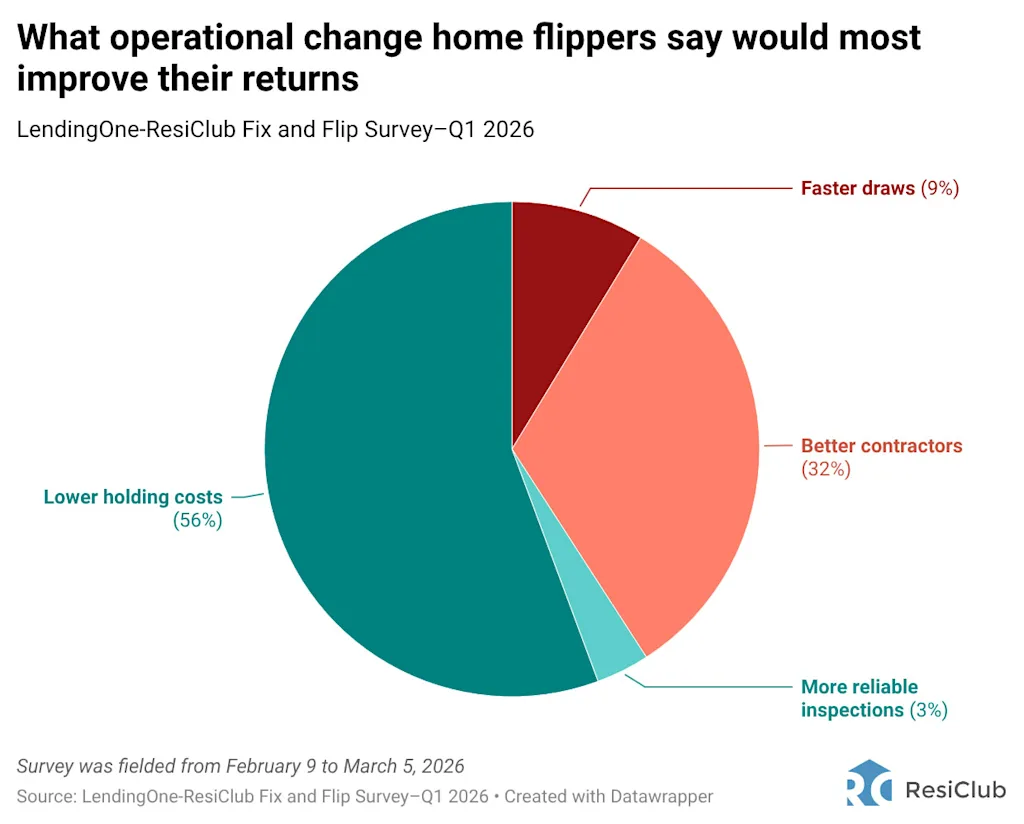

- Lower holding costs would most improve returns according to 56% of flippers, followed by better contractors (32%), faster draws (9%), and more reliable inspections (3%).

Let’s view the full results