Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

Speaking at the Bank of America Housing Symposium in June 2025, Toll Brothers CEO Doug Yearley—who has since stepped down—acknowledged that parts of Arizona, Florida, and Texas were dealing with spec inventory “overhangs” that he said would eventually “clean up [over time] because the builders are starting fewer spec homes in the softer market, and I think that will naturally work its way out.”

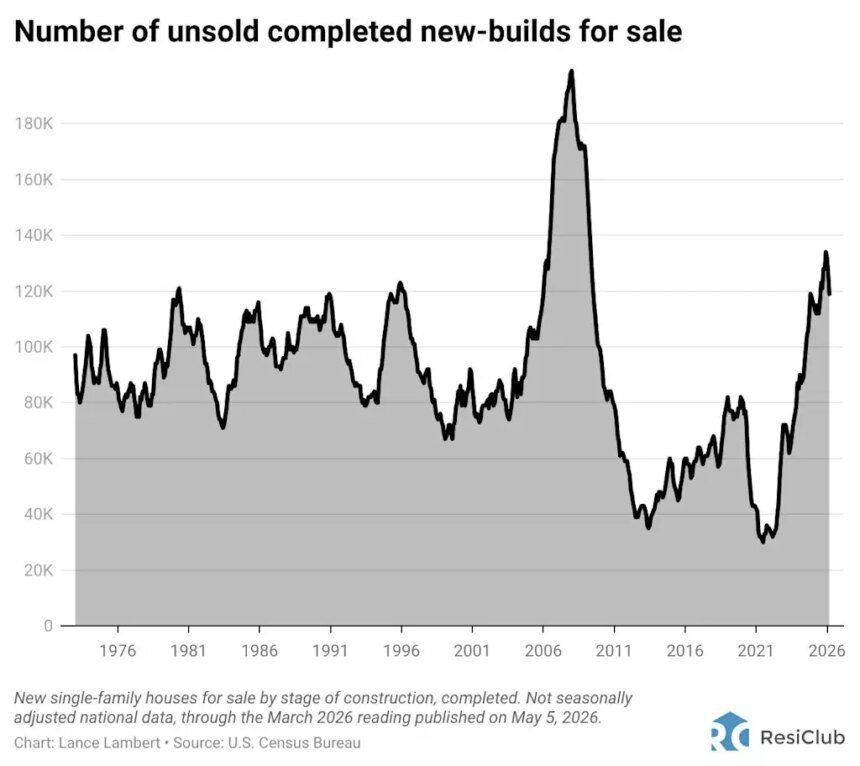

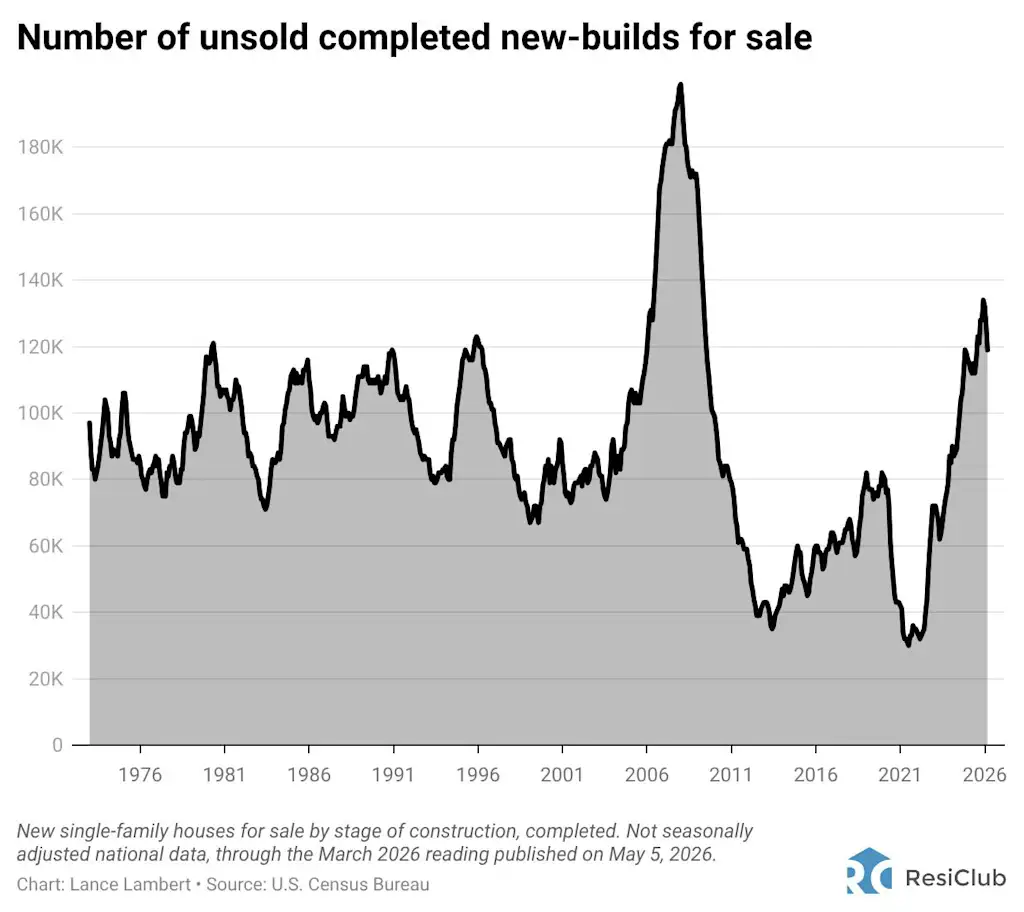

At the height of the pandemic housing boom, when nearly everything homebuilders were building was flying off the shelves, there were only 32,000 unsold completed new-build homes in March 2022. Once the boom fizzled out, that figure quickly began to rebound—especially in Sunbelt boomtowns—reaching a high of 134,000 unsold completed new-build homes by December 2025.

However, data published this week shows that the number of unsold completed new-build homes has, at least for now, fallen to 119,000 as of March 2026. While the count of unsold completed new-build homes is still up year over year (there were 113,000 unsold completed in March 2025), the decline over the past few months has been larger than seasonality alone would suggest.

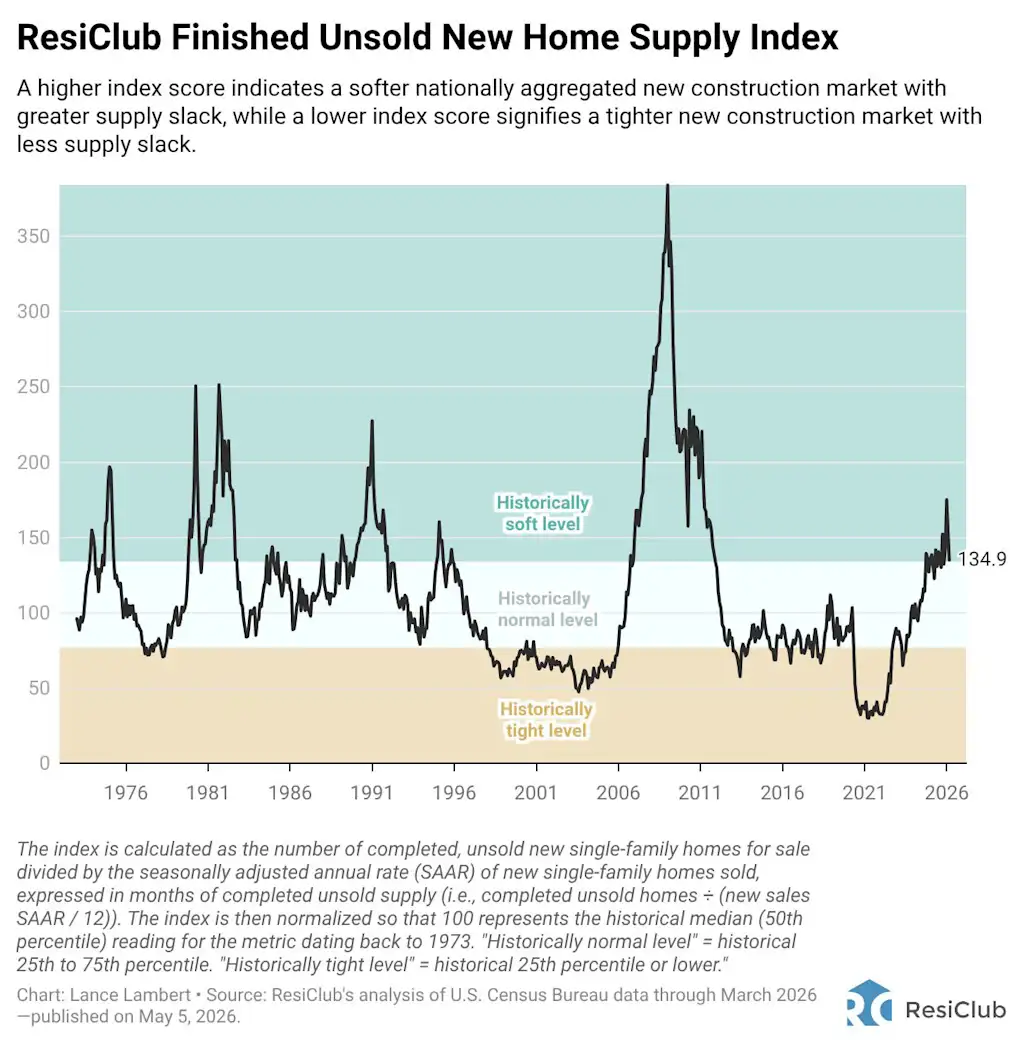

To put the number of unsold completed new single-family homes into better historic context, we have the ResiClub Finished Unsold New Homes Supply Index. It accounts for unsold completed inventory relative to new home sales. A higher index score indicates a softer national new construction market with greater supply slack, while a lower index score signifies a tighter new construction market with less supply slack. Over the past few months, that reading has almost drifted back down into the “historically normal” range.

After experiencing a softer 2025 than expected—and greater-than-expected margin compression—many giant homebuilders told analysts heading into 2026 that they’d pivot toward fewer spec builds and more build-to-order homes. The reason was simple: Build-to-order margins are materially higher. Built-to-order homes tend to generate higher margins because they’re sold before construction begins, reducing inventory carrying costs and the risk of having to deploy larger incentives to sell them.

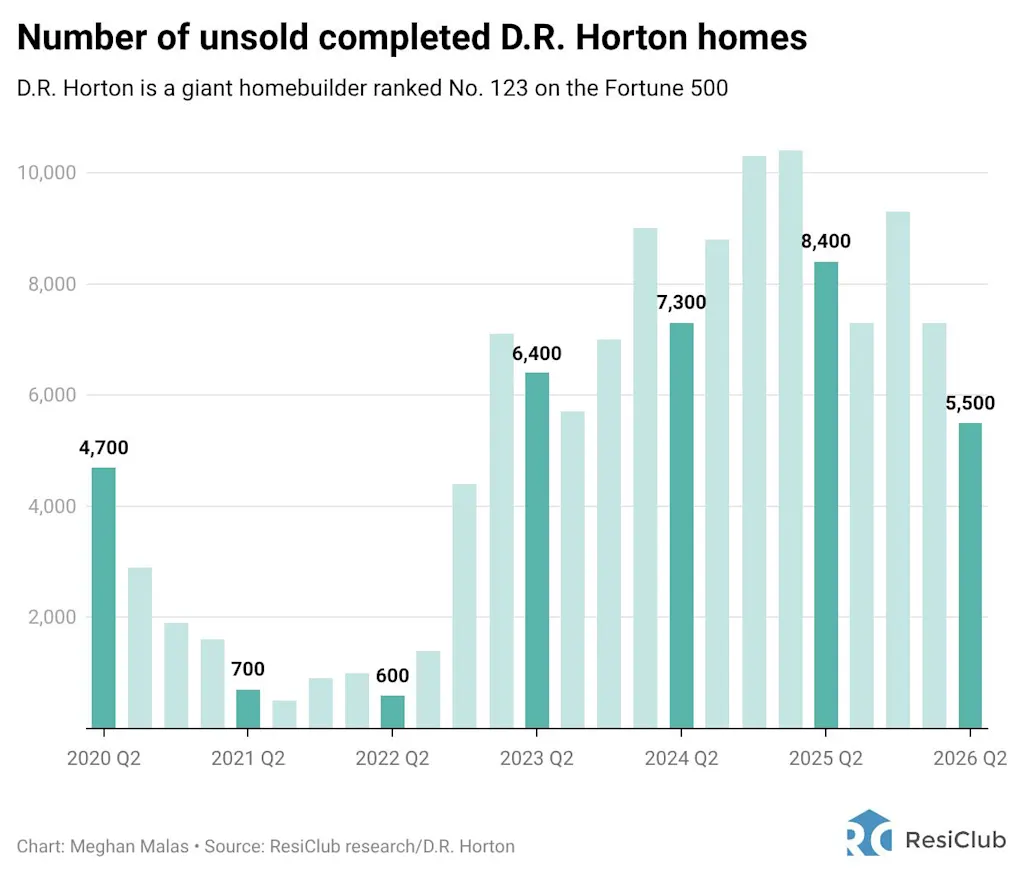

Doing fewer specs and starts in softer pockets of the Sunbelt has already helped some of the builders reduce their count of unsold completed homes. Just look at America’s largest homebuilder, D.R. Horton.

Here’s what Paul Romanowski, CEO of D.R. Horton, said during the company’s April 21, 2026 earnings call:

“Unsold homes [for us] are down 25% from December and 35% from a year ago, with both unsold homes as a percentage of total inventory and completed unsold inventory at their lowest levels since fiscal 2023 for homes closed in the second quarter.

“We expect starts in the third quarter to be lower than the second quarter, and we will continue to manage our inventory levels and start space based on market conditions.”

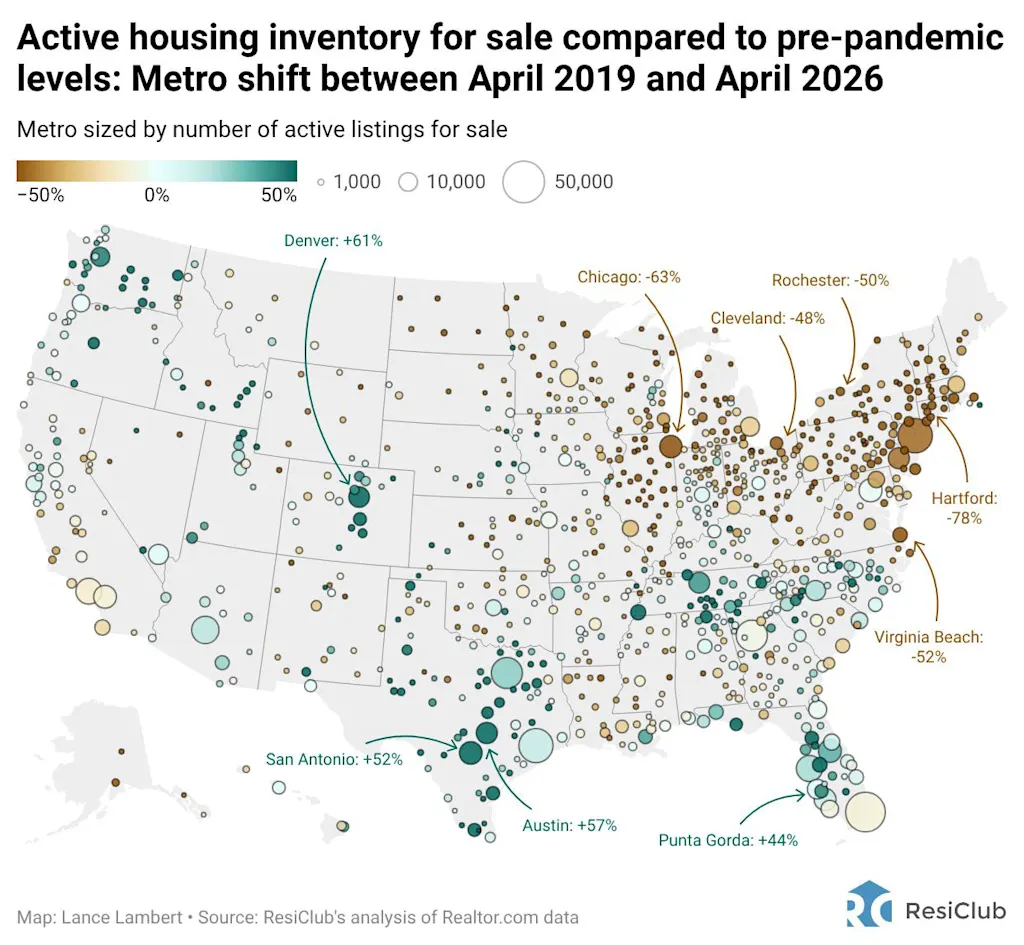

While the U.S. Census Bureau doesn’t give us a greater market-by-market breakdown on these unsold completed new builds, we have a good idea where they are, based on total active inventory homes for sale (including existing)—likely much of it is in the Mountain West and the Sunbelt, particularly around the Gulf.

We should point out that while many markets in Texas and Florida experienced a significant post–pandemic housing boom inventory bounce-back, that inventory growth has decelerated in recent months. In fact, many parts of Florida are now seeing year-over-year active inventory for sale declines. The heavy discounting by homebuilders in weaker pockets of Texas and Florida to move unsold inventory—combined with reduced housing starts and fewer spec builds in those pockets heading into 2026—has, in part, contributed to that slowdown in inventory growth.

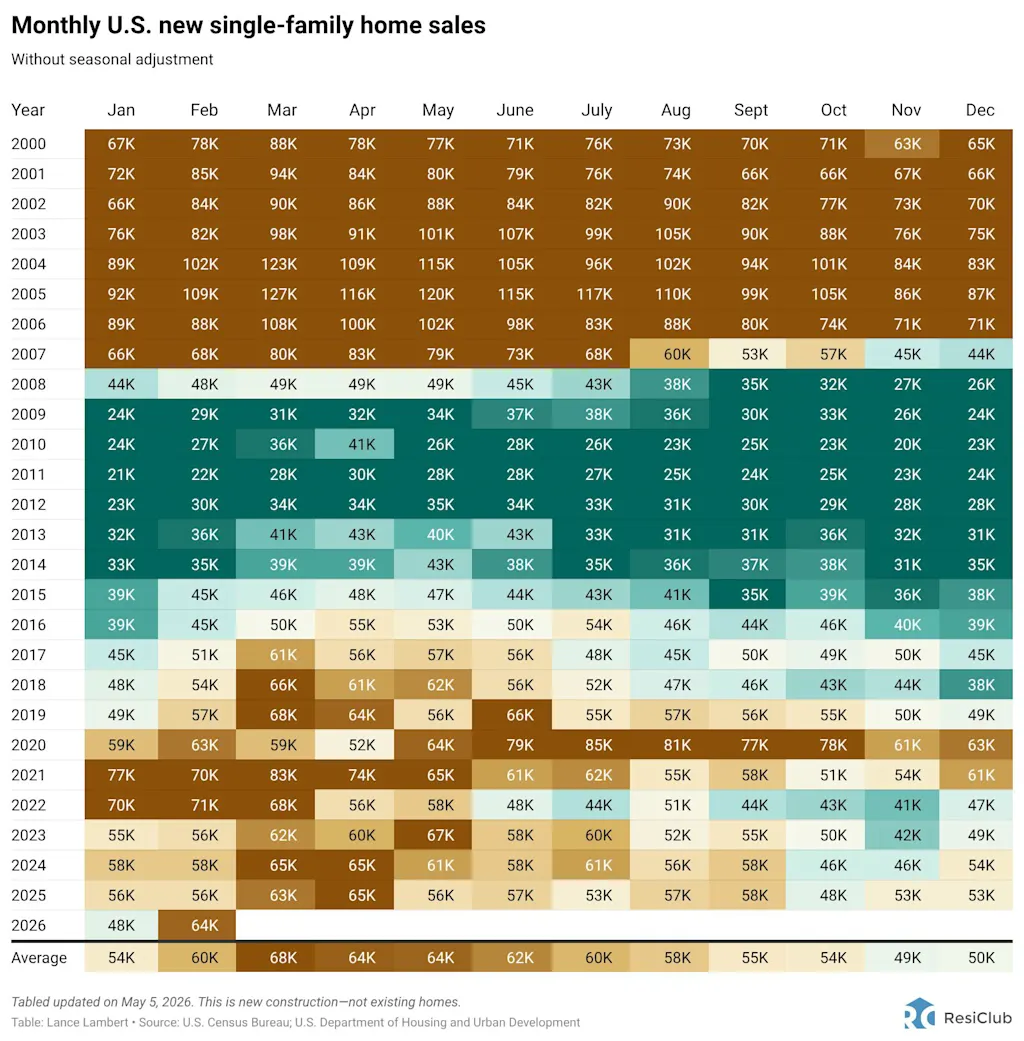

Unlike the existing-home market—where U.S. existing-home sales are still -23.6% below pre-pandemic 2019 levels—U.S. new-home sales are essentially on par with pre-pandemic 2019 levels right now 👇

Why haven’t U.S. new home sales come down more, given the affordability picture and what’s happened in the existing-home market?

A lot of it boils down to the fact that many homebuilders since the pandemic housing boom fizzled out have done larger affordability adjustments—including everything from bigger buydowns, more money back at close, and even outright price cuts—in order to keep moving product when they run into softness in a given neighborhood. The most aggressive homebuilder on the incentive front is Lennar. Last quarter, Lennar spent the equivalent of 14% of the final sales price on sales incentives. For a $400,000 home, that translates to $56,000 in incentives. Lennar’s cycle low was in Q2 2022, when it spent 1.5% of the final sales price on sales incentives.

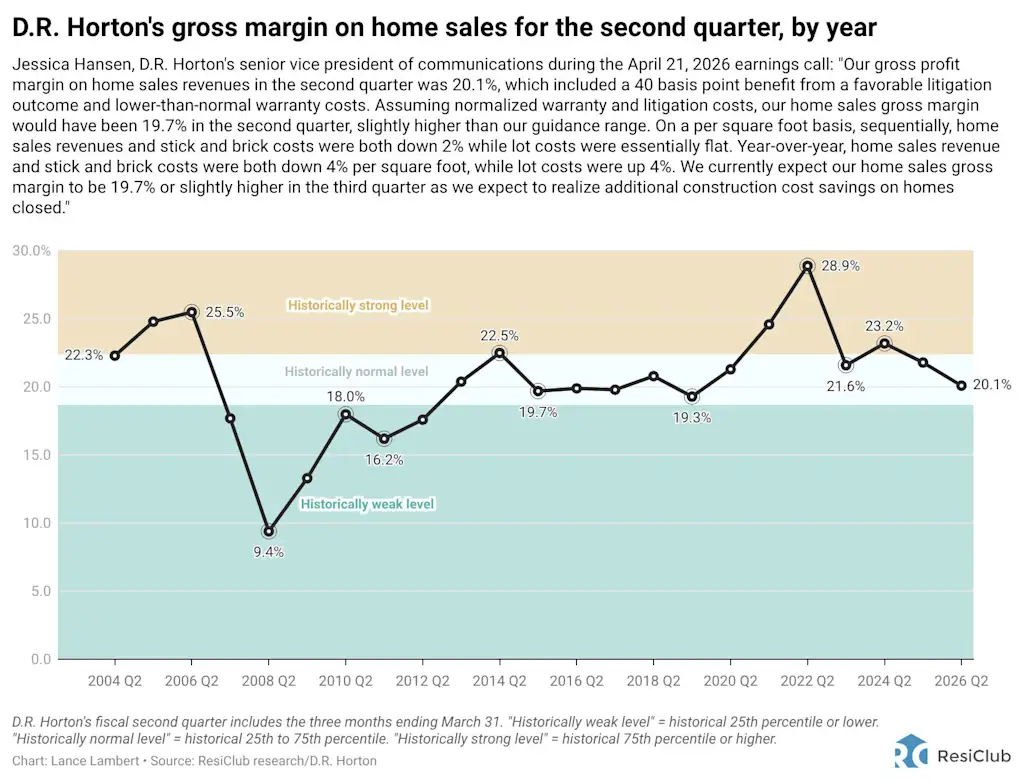

In order to do bigger incentives—and pay for sticky land prices—homebuilders have been compressing margins. Indeed, all 11 of the major publicly traded U.S. homebuilders that ResiClub tracks the most closely have seen year-over-year gross margin compression.

So in other words, big homebuilders have been willing to adjust prices and incentives in order to maintain sales volume, while existing-home sellers, in aggregate, have fought harder against price adjustments—at the expense of speed of sale and turnover. Another factor is that homebuilders’ willingness to sell isn’t impacted by so-called affordability “lock-in.” Ever since mortgage rates spiked, high switching costs have left many homeowners either unwilling or unable to sell and buy at today’s prices and rates, further suppressing existing-home turnover.

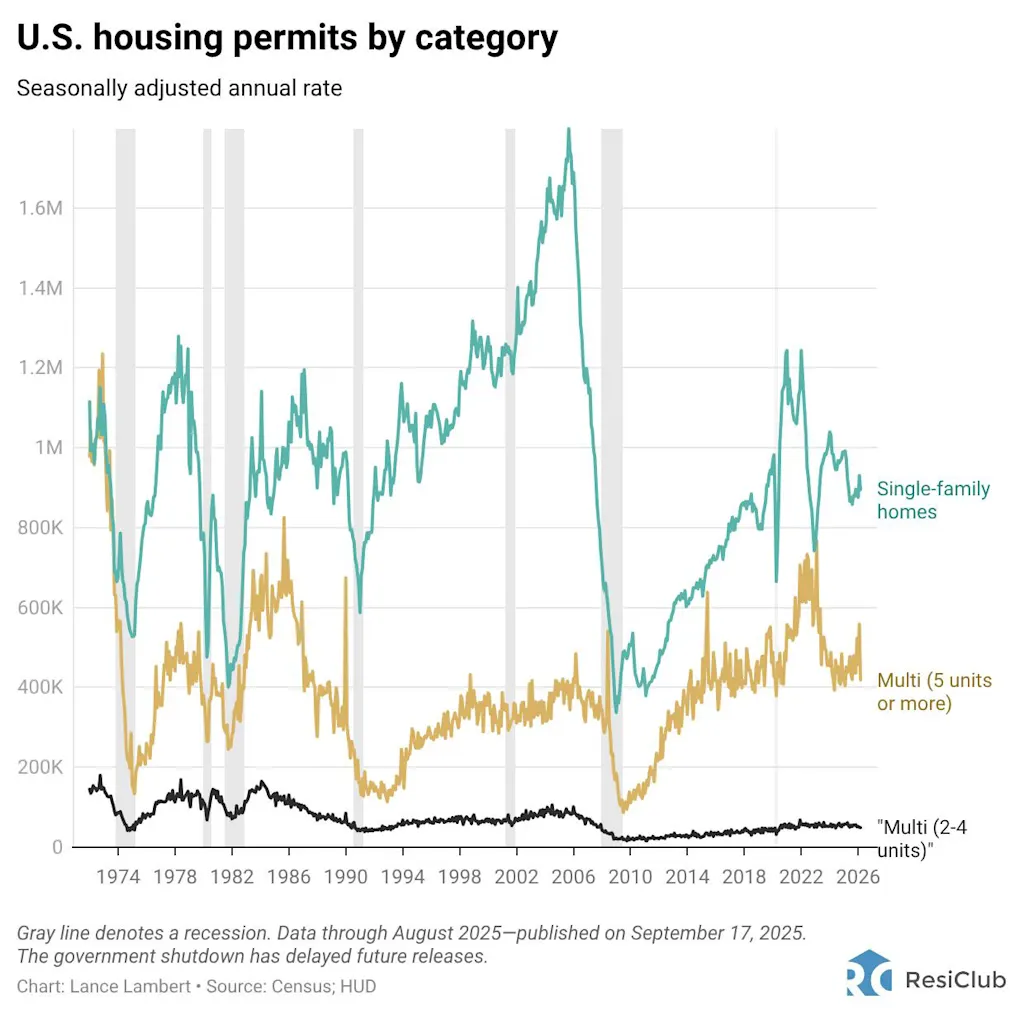

Before we conclude today’s new construction report, here’s a historic look at nationally aggregated permits.