Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

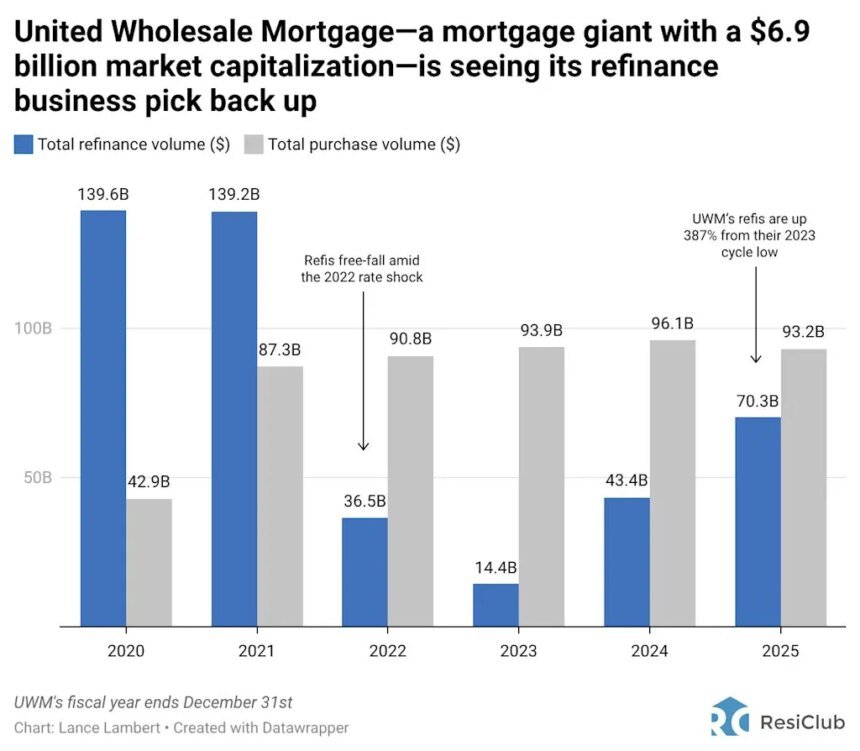

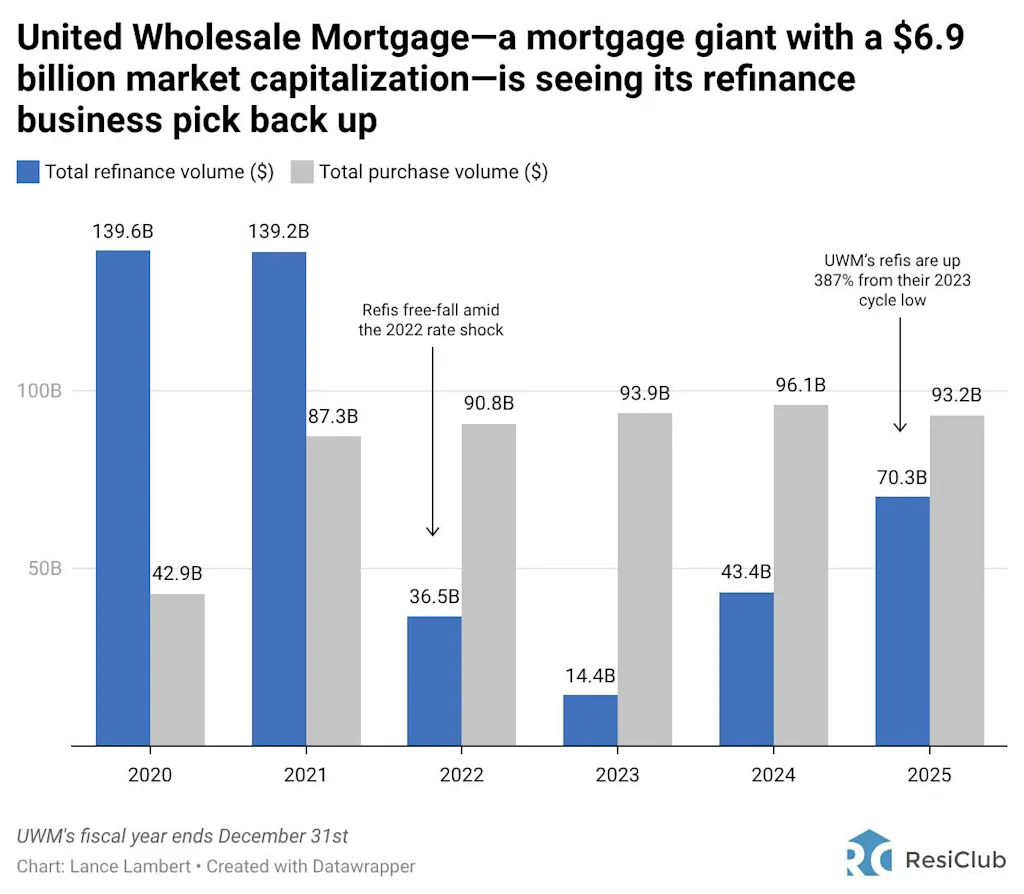

After taking a big macro hit during the 2022 rate-shock, United Wholesale Mortgage’s (UWM) refinance volume has found its footing—and keeps climbing:

- 2020: $140B

- 2021: $139B

- 2022: $36B

- 2023: $14B (cycle low)

- 2024: $43B

- 2025: $70B

That’s a +387% increase in UWM’s refi volume since its 2023 cycle low.

Even without a full refi boom, refinance volume is slowly coming back, with the average 30-year fixed mortgage rate as tracked by Freddie Mac down to 5.98% last week—or 1.81 bps below its cycle high of 7.79% in October 2023.

Many recent borrowers who took on higher mortgage rates (2023–2024 vintages) are jumping at the opportunity to refinance and secure some payment relief. At the same time, UWM’s purchase volume has remained relatively steady in the $90B–$96B range over the past few years.

The lack of a sharp decline in purchase volume following the rate-shock is impressive when you consider the macro picture: While U.S. existing home sales fell sharply in 2022, UWM’s purchase volume held steady as the wholesale channel gained share during the downturn. Many smaller lenders pulled back or exited, and brokers consolidated volume toward large, price-competitive players. UWM kept pushing forward. That purchase stability gives UWM a great base to operate from as refis improve.

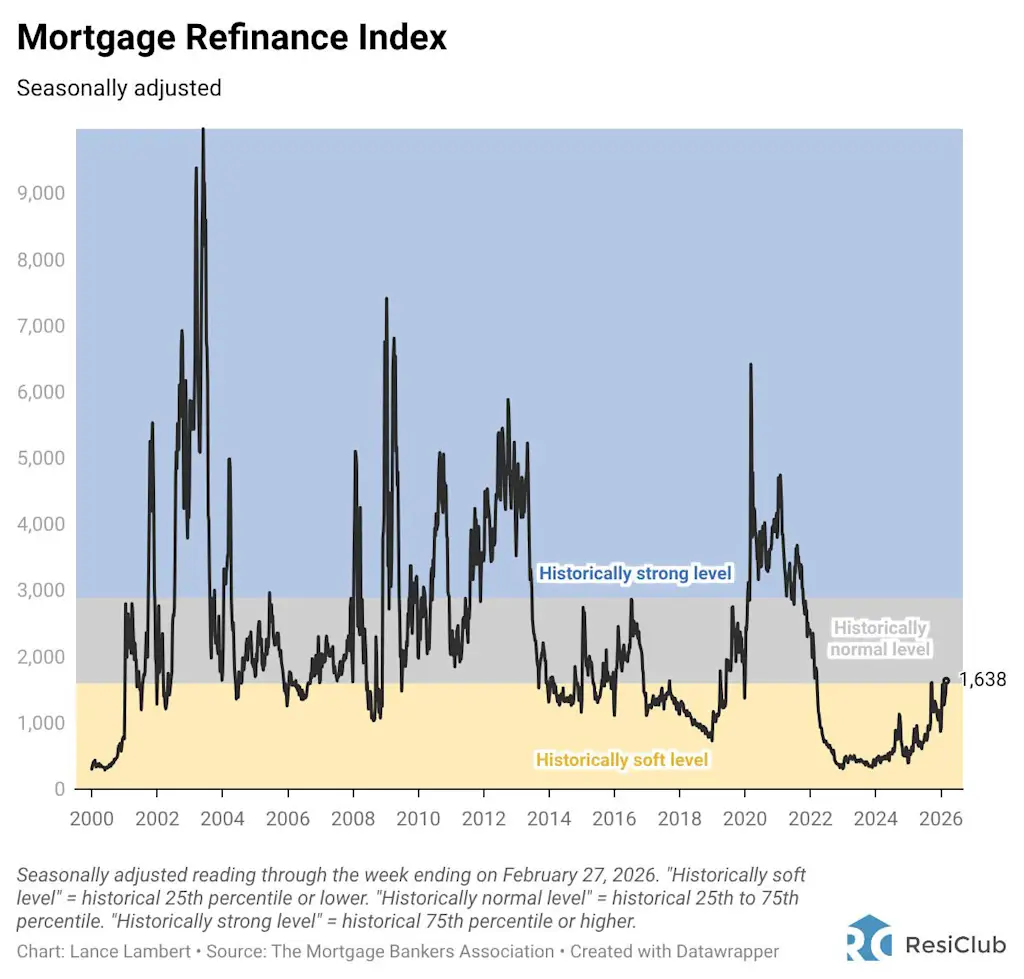

While UWM’s refinance rebound is happening faster than most mortgage firms (and as a result, it’s taking refinance market share), refinance activity overall is slowly bouncing off the rate-shock lows.

The Mortgage Refinance Index reading for the fourth week of February, by year:

- February 2018 —> 1,169

- February 2019 —> 1,134

- February 2020 —> 3,594

- February 2021 —> 3,850

- February 2022 —> 1,686

- February 2023 —> 400

- February 2024 —> 396

- February 2025 —> 784

- February 2026 —> 1,638

Zoomed out, mortgage refinance applications started 2026 still in “historically soft” territory (bottom 25th percentile). However, over the past week, they crossed the threshold into the bottom of “historically normal” refinance levels (25th–75th percentile).

ResiClub prefers to call this upswing a “refi boomlet” rather than a “refi boom.” We use the term boomlet because there’s a ceiling on how big this refinance pop can get—and how long it can last—without a more substantial drop in mortgage rates. After all, according to the latest FHFA data, 68.6% of U.S. mortgage borrowers still hold an interest rate below 5.0%.

That said, the more time U.S. homeowners have to adjust to today’s mortgage rates, the more some may be enticed to refinance or tap their equity through a HELOC or home equity loan.