Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

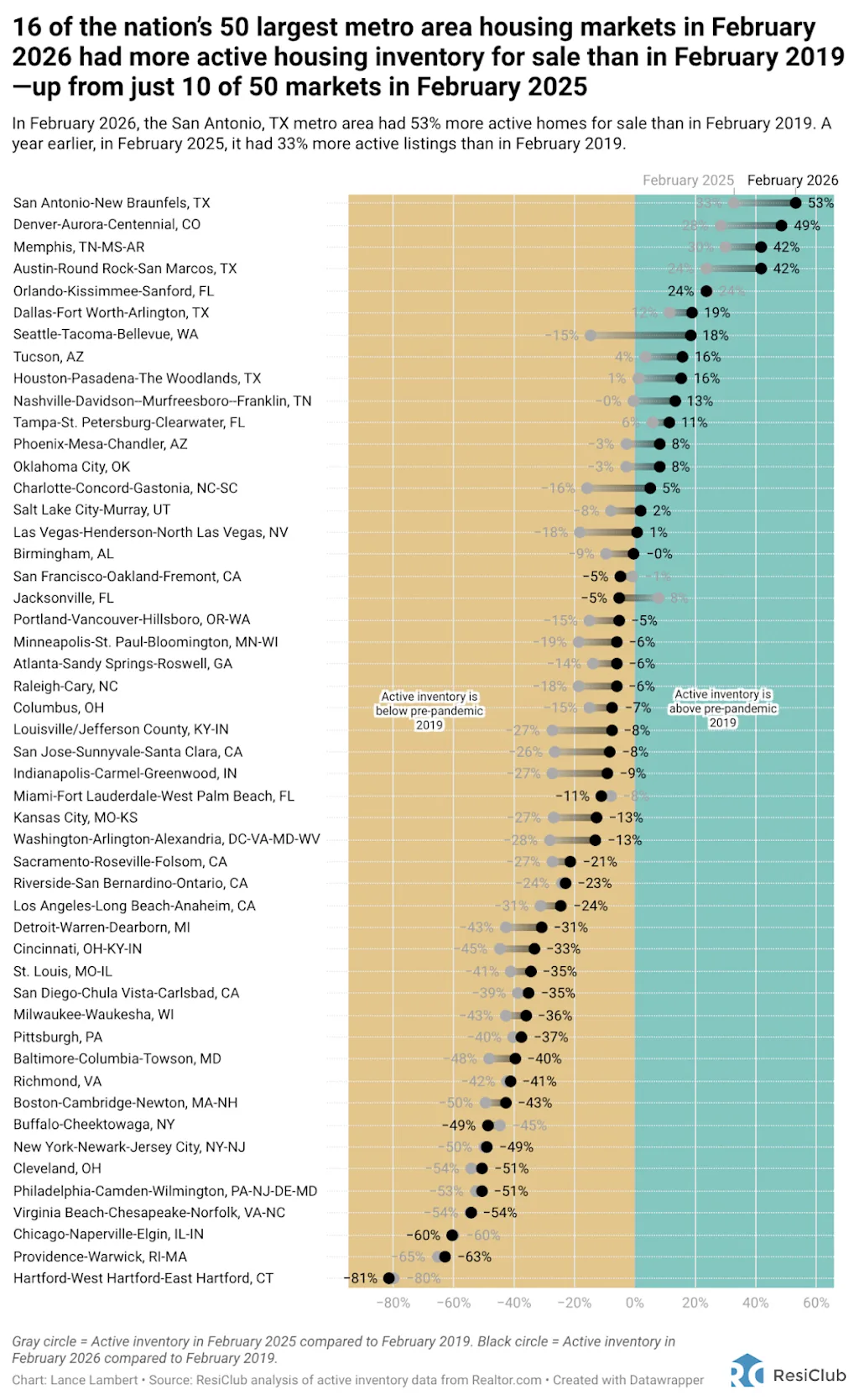

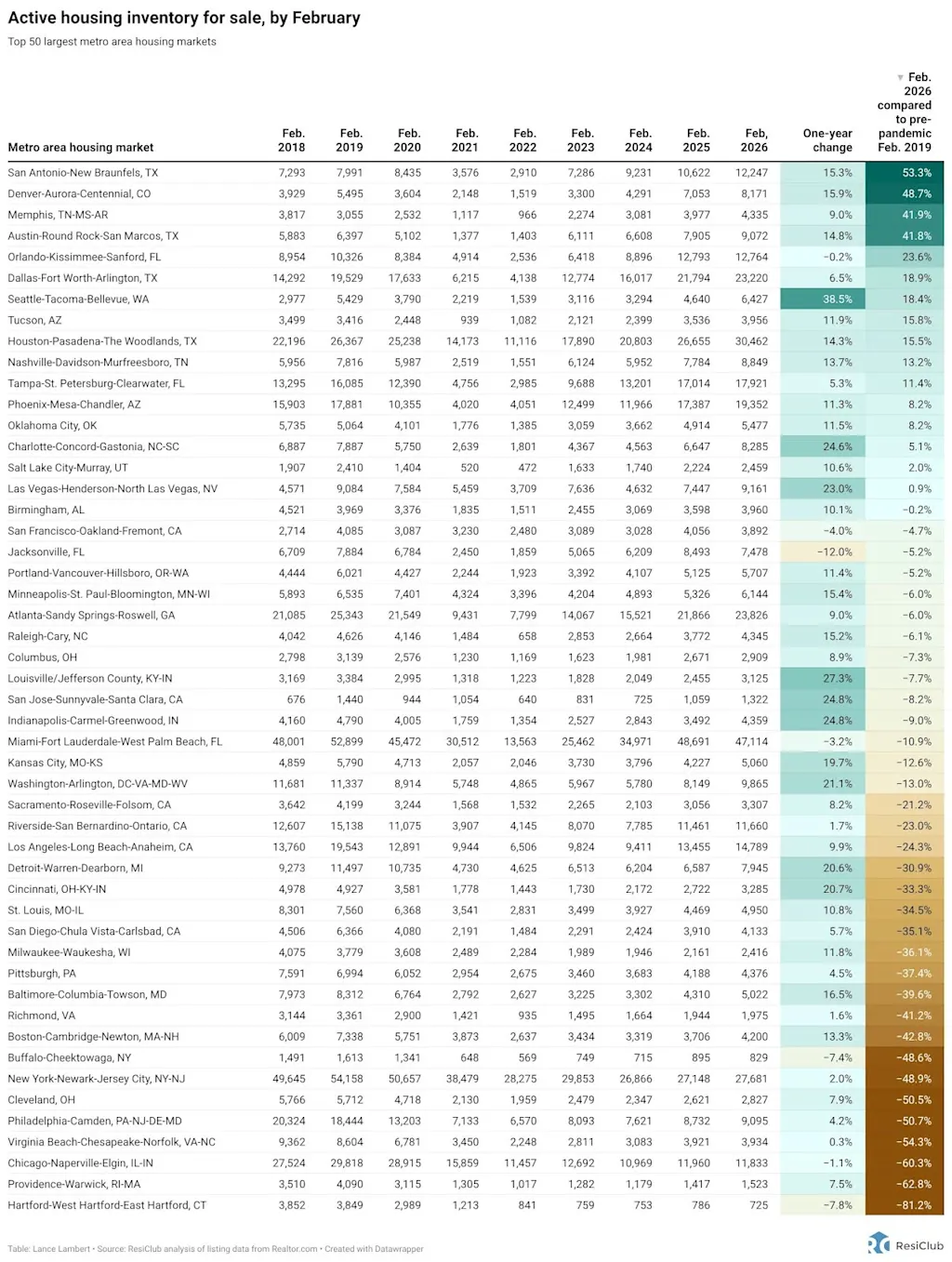

While active listings are rising year-over-year in most regional housing markets, a slight majority of markets are still below pre-pandemic 2019 inventory levels.

Generally speaking, housing markets where inventory (i.e., active listings) has returned to pre-pandemic 2019 levels have experienced weaker home price growth (or outright declines) over the past 42 months. Conversely, housing markets where inventory remains far below pre-pandemic 2019 levels have, generally speaking, experienced more resilient home price growth over the past 42 months.

Many of the softest housing markets, where homebuyers have gained the most leverage since the Pandemic Housing Boom ended, are located in Southern and Mountain West regions. Many of those areas were home to many of the nation’s top pandemic boomtowns, which experienced significant home price growth during the Pandemic Housing Boom, which stretched housing prices beyond local income levels.

Once pandemic-fueled domestic migration slowed and mortgage rates spiked, markets like Punta Gorda, Florida, and Austin, Texas, faced challenges as they had to rely on local incomes to sustain frothy home prices.

The housing market softening in these areas was further accelerated by the abundance of new home supply in the pipeline across the Sun Belt. When and where needed, builders are often willing to reduce prices or make other affordability adjustments to maintain sales. These adjustments in the new construction market also create a cooling effect on the resale market, as some buyers who might have opted for an existing home shift their focus to new homes where deals are available.

In contrast, many Northeast and Midwest markets were less reliant on pandemic domestic migration and have less new home construction in progress. With lower exposure to that migration pullback demand shock—and fewer homebuilders doing large incentives—active inventory in these Midwest and Northeast regions has remained relatively tight.

window.addEventListener(“message”,function(a){if(void 0!==a.data[“datawrapper-height”]){var e=document.querySelectorAll(“iframe”);for(var t in a.data[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.source){var d=a.data[“datawrapper-height”][t]+”px”;r.style.height=d}}});

Although active inventory is rising year-over-year, much of the Midwest and Northeast remain below pre-pandemic 2019 inventory levels. In contrast, many parts of the Gulf Coast, including Tampa and Atlanta, and the Mountain West have ticked back above pre-pandemic 2019 inventory levels.

Among major markets, home sellers in markets like Hartford and Chicago have retained more leverage/power.

Among major markets, homebuyers in markets like Tampa, Denver, and Austin have gained more leverage/power.

In total, 16 of the nation’s 50 largest metro area housing markets are entering the spring 2026 selling season with more active inventory than they had in pre-pandemic 2019. Those markets include San Antonio, TX; Denver, CO; Memphis, TN; Austin, TX; Orlando, FL; Dallas, TX; Seattle, WA; Tucson, AZ; Houston, TX; Nashville, TN; Tampa, FL; Phoenix, AZ; Oklahoma City, OK; Charlotte, NC; Salt Lake City, UT; and Las Vegas, NV.

Here’s what Phillippe Lord, CEO of Meritage Homes, said on the company’s January 29, 2026 earnings call:

“In Q4, demand patterns were highly localized by market with a generally tougher selling environment nationwide. Across all regions, incentive utilization increased to get buyers off the fence. In our most favorable markets, Dallas, Houston, North and South Carolina, we maintained a strong absorption pace supported by resilient local economic conditions. Conversely, our teams faced lower demand and aggressive local competition in Austin, San Antonio, parts of Florida, Northern California and Colorado. We deliberately chose to hold our ground in these markets and accept lower sales volumes as we look to the spring selling season to work through our excess home inventory.”

That said, in some pockets of relatively higher-inventory markets (such as pockets of Dallas and even Cape Coral), some homebuilders have firmed up sales if they’ve already made the necessary pricing and incentive adjustments to meet the market. As is always the case in real estate, at the ground and neighborhood level there can be a tremendous amount of nuance.