Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

John Rogers, the chief data and analytics officer of Cotality (formerly known as CoreLogic), returned to ResiDay this year to give a two-part presentation: first, how risk—insurance, climate, construction cost—is reshaping the housing market, and second, how AI is about to turn property professionals into “superheroes.”

In 2011, the firm was predominantly a U.S. mortgage-data company. Today, Cotality is a multicountry, multi-industry analytics platform that supports more than 1 million real estate agents, touches more than 8 out of every 10 U.S. mortgages, and interacts with a similar share of property insurance policies. Across those businesses, Cotality collects data from 22,000 unique sources—from county recorders to satellite imagery to lidar scans on smartphones.

“I’m fortunate to look after this 21st-century data and AI manufacturing plant,” Rogers told the audience. He manages a team of about 200 data scientists and meteorologists.

Insurance premiums reach a record share of monthly payments

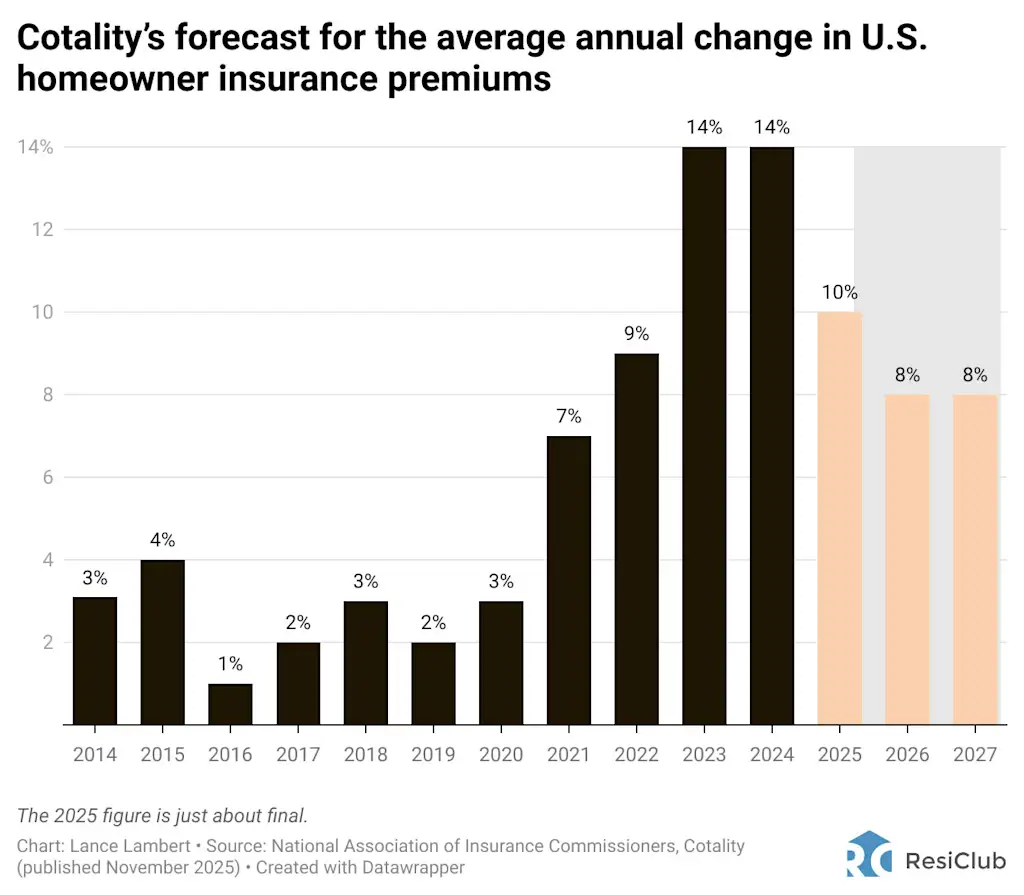

Insurance now accounts for 9% of the typical U.S. homeowner’s payment—the highest share on record, according to Cotality. Several states have seen double-digit premium increases in just the past year.

Looking ahead, Cotality expects average annual U.S. homeowner insurance premiums to rise another 8% in 2026, followed by an additional 8% increase in 2027.

According to Cotality, three forces are putting upward pressure on home insurance.

First, there’s rising construction and material costs. Cotality tracks the exact reconstruction cost for every property in the country—“every nail and two-by-four.” During the Pandemic Housing Boom, there was historic overheating in both home prices and material prices, which has led to higher replacement costs. That’s still feeding into higher home insurance premiums.

Second, more homes are facing climate-related hazards. Roughly 12% of today’s U.S. housing stock sits in high-risk hazard zones (wildfire, winter storm, hail, and flooding) representing $4.3 trillion in hypothetical reconstruction costs. By 2050, that share rises to 20%, or $7.2 trillion. Cotality models the financial impact of each hazard on every property, giving insurers—and, increasingly, homeowners—risk scores that account for both current and future conditions.

Third, there’s migration into high-risk areas. The densification of the U.S. housing stock mirrors the growth of homes in hazard-prone regions. “One in six Americans now lives in a high-wildfire-risk area,” Rogers noted. Florida and Georgia, which experienced rapid population growth, are among the states most exposed.

After outlining why home insurance premiums are rising, Rogers turned to how science and data can reduce losses—and premiums.

Urban conflagration drove the Los Angeles losses, he said. Despite relatively low wildfire-risk scores, neighborhoods in the Palisades burned because of building-to-building ignition. Cotality is now modeling this “urban conflagration” risk at the individual-property level, giving insurers a clearer view of how fires spread across aging housing stock.

Rogers added that rebuilding communities like Palisades for a safer future can help contain premiums. He said that following the 2018 Palisades fire, Cotality helped design a rebuilding blueprint that could reduce wildfire risk by up to 75%, and cut insurance premiums by more than 50%. The blueprint included IBHS-standard hardened homes, redesigned lower-density layouts with fire breaks, and risk-mitigation strategies around community perimeters.

Finally, Rogers said that premiums can be lowered through home-level resilience assessments. Cotality worked with the California Department of Insurance to evaluate every home using aerial imagery and AI. Attributes such as roof materials, closed eaves, setbacks, and nonflammable defensible space feed into resilience scores that insurers use to cut premiums by 20% or more.

These resilience assessments are now being deployed beyond California, he said. One striking example: Seminole County, Georgia—far from coastal hazards—has six times the risk level of hardened-home counties in Florida, underscoring the power of building codes.

The final deadline for Fast Company’s World Changing Ideas Awards is Friday, December 12, at 11:59 p.m. PT. Apply today.