Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

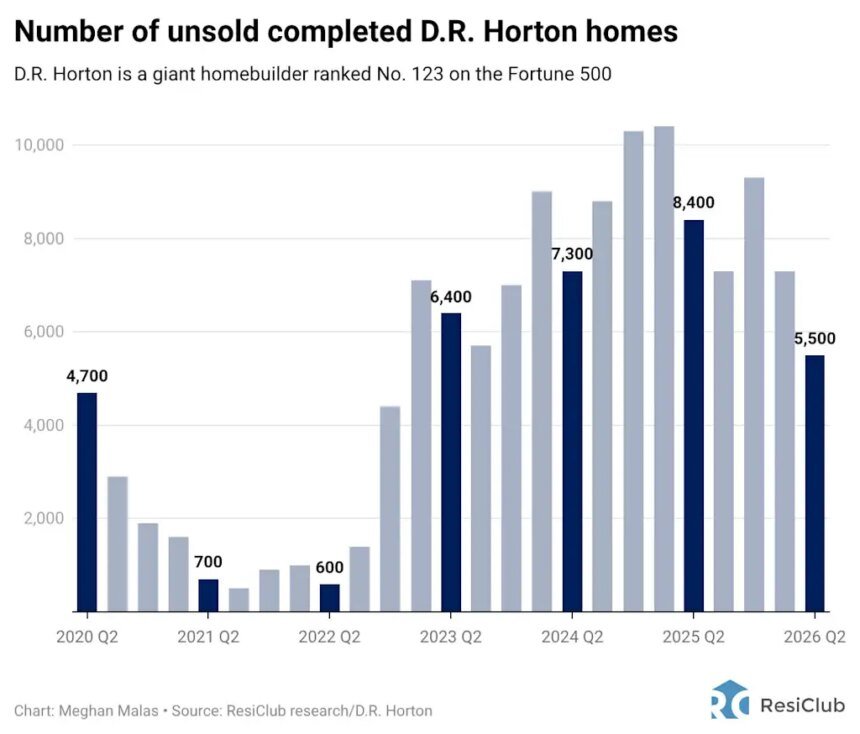

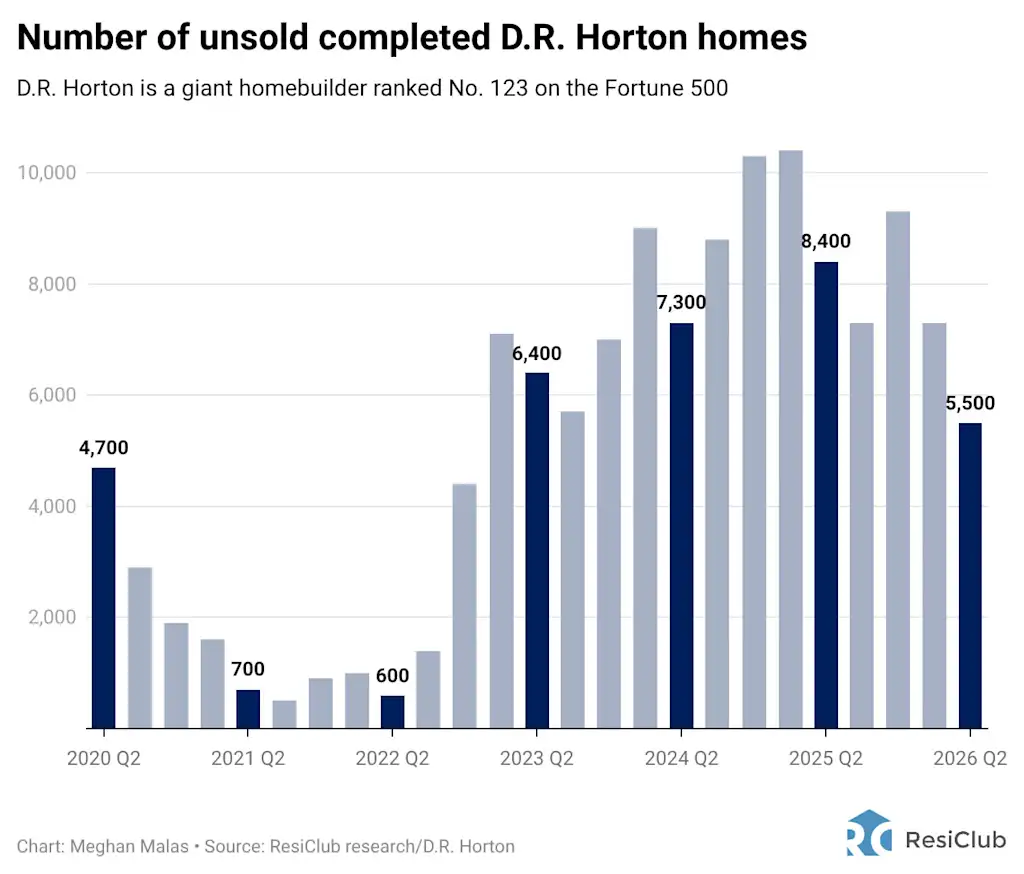

During the pandemic housing boom, homebuilders saw their number of unsold completed new builds dry up as overheated demand quickly absorbed almost everything for sale. That is exactly what was experienced by D.R. Horton, America’s largest homebuilder, which had just 600 unsold completed new builds for sale in fiscal Q2 2022—compared to 4,700 in its fiscal Q2 2020.

However, as the pandemic housing boom ended and the market shifted, U.S. homebuilders saw their unsold new builds spike back up. At the end of its fiscal Q2 2025—the three months ending March 31—D.R. Horton had 8,400 unsold completed.

Fast-forward to fiscal Q2 2026, and D.R. Horton has shrunk its unsold completed inventory to 5,500 as it’s worked to move unsold inventory and balance sales pace with current “market conditions.” This matters because unsold completed homes are a drag on margins: The longer a finished home sits, the higher the carrying costs, and the more the company may need to discount it to move it.

“Unsold homes are down 25% from December and 35% from a year ago, with both unsold homes as a percentage of total inventory and completed unsold inventory at their lowest levels since fiscal 2023 for homes closed in the second quarter,” CEO Paul Romanowski said during D.R. Horton’s April 21 earnings call. “We expect starts in the third quarter to be lower than the second quarter, and we will continue to manage our inventory levels and start space based on market conditions.”

How was D.R. Horton able to achieve this drawdown in unsold completed inventory?

Given the increased softness last year across many pockets of core homebuilding markets in the Sunbelt—in particular in pockets of Florida and Texas—D.R. Horton slowed its spec starts heading into 2026. That has helped it reduce the number of unsold completed builds on its books.

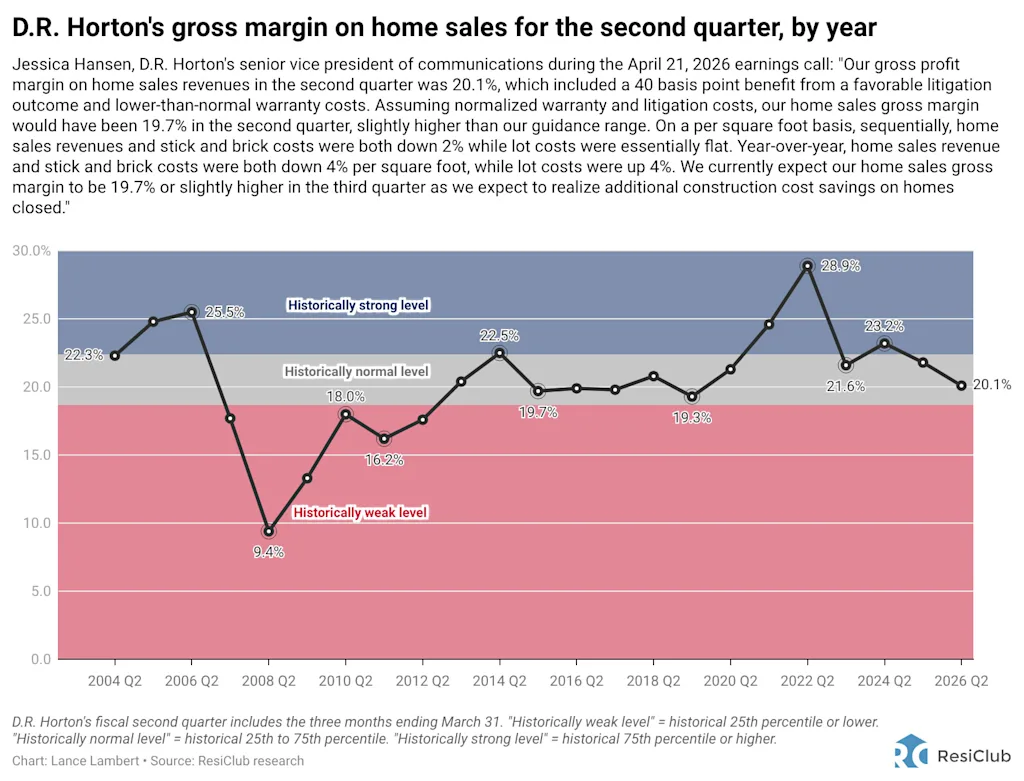

The company further compressed its gross margin in order to do bigger affordability adjustments and sales incentives—like mortgage rate buydowns—to help entice buyers and move the completed unsold new builds.

“Our sales incentives increased during the second quarter, and we expect incentives to remain elevated for the rest of the year,” Romanowski said on the earnings call, noting that the incentives as a percent of revenue are roughly 10%.

A sales incentive rate of 10% is fairly high. Many homebuilders run sales incentive rates closer to 4% to 6% during balanced supply-demand periods.

“We currently expect our home sales gross margin to be 19.7% or slightly higher in the third quarter as we expect to realize additional construction cost savings on homes closed,” Jessica Hansen at D.R. Horton told analysts during the earnings call.

The higher incentive rate helped D.R. Horton boost its net new orders by 11% year over year.

Another factor behind D.R. Horton’s decline in unsold completed homes is that while some of its largest markets remain soft, the pace of that softening has eased over the past eight months. Inventory is no longer surging as quickly across many Sunbelt markets. Had the sharp softening seen in the second half of 2024 and first half of 2025 persisted into 2026, D.R. Horton would likely be carrying a larger stock of unsold completed homes today.

“I think we’re seeing good demand in Texas, consistent as well. In Florida, the markets feel pretty good to us. Generally across the country, I would say that most of our markets are performing well in line with expectations,” COO Michael Murray said during the company’s earnings call. “Perhaps [there’s] a little bit of softness, and a few of our markets that have kind of a traditionally heavy exposure to the software industry, that buyers sentiment may be off a bit. Other than that, just kind of a good, good start to spring. Pretty encouraged.”

Big picture: Unsold completed homes are a drag on homebuilder margins. The longer a finished home sits, the higher the carrying costs—and the more the company may need to discount it to move it. Right now, in softer pockets of the housing market—particularly in many pandemic boomtowns across Florida, Arizona, Colorado, and Texas—homebuilders are offering sizable incentives. But if they’re able to further reduce their number of unsold completed homes, they may become less willing to offer even juicier incentives to move product.